Skip to main content

Skip to main content

A new trade era: market volatility after ‘Liberation Day’

It is quite remarkable what can happen over a 90 day period. Entering the year investors were optimistic that pro-growth policies in the US and the prospect of interest rate cuts would support global growth and drive the price of risk assets higher.

Arrange your free initial consultation

Trepidation emerged on the 20th January with the inauguration of President Trump and the promotion of what he and his administration considered ‘America First’ policies. Despite suggestions that this would be transitory, the initial tariffs on the imports of goods from Canada, Mexico and China proved enough to shake US equity markets. After reaching an all-time high in late February, the S&P 500 would end the quarter down 4.1%.

This uncertainty saw countries across the world reappraise their relationship with the US and question whether it would continue to be the global steward.

Nowhere was this more notable than in Europe, where we saw the announcement of significant fiscal packages, including an €800bn commitment from the European Commission to develop the region’s defence capabilities. More seismically, Germany – a country which typically has forgone mass fiscal programs – announced a €500bn infrastructure plan.

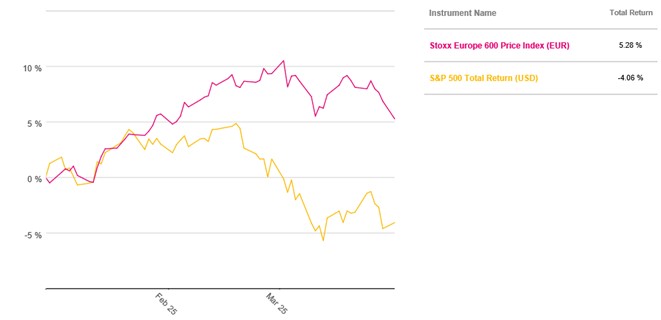

Already benefitting from a combination of cheap valuations and improving investor sentiment, this announcement saw European equities climb higher in February as US equities fell.

Figure 1: Outperformance of European Equities vs US Equities in Q1 (Source: Pacific Asset Management)

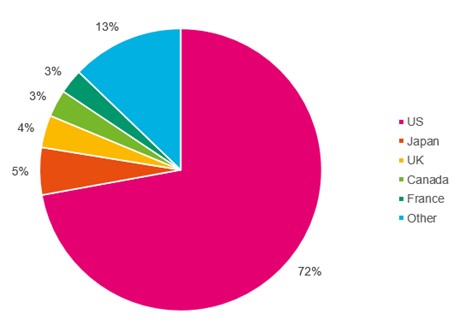

This proved a challenging period for investors with a relatively large allocation to US equities. For example if we take a typical global equity index portfolio, where each country is allocated a weight based on its market capitalisation (size of equity market), then you can see that the allocation to US equites would be more than 70% (see Figure 2.).

Figure 2: MSCI World Global Equity Allocation (Source: MSCI)

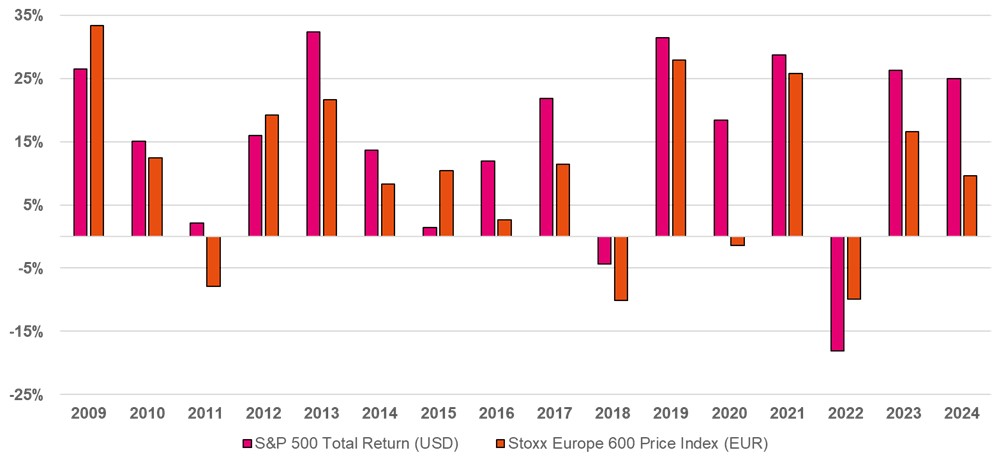

This, of course, would have previously been a highly successful strategy (‘buying the market’) because post 2008 in the era of cheap credit and increased liquidity, US equities only failed to outperform European equities on just four occasions (see Figure 3.).

Figure 3: US equities vs European Equities 2009-2024 (Source: Pacific Asset Management)

These strategies do well when the status quo remains and there are no structural changes to the world order. However the rule book of global trade appears to have changed and rather than being a short lived measure, US tariff policy appears to be an entrenched position heralded by President Trump’s so-called “Liberation Day”.

President Trump declared the 2nd of April as Liberation Day, which signalled a seismic shift in US trade policy. This saw the instigation of a 10% base tariff for every country (regardless of the trade position with the US) along with reciprocal tariffs which looked to target those countries which were considered to have been taking advantage of the US either through large trade imbalances or applying high tariffs to the import of US products.

These tariff rates were above market participants forecasts – the full list can be seen below:

Figure 4: New US tariff rates (Source: GMK Centre, 2025)

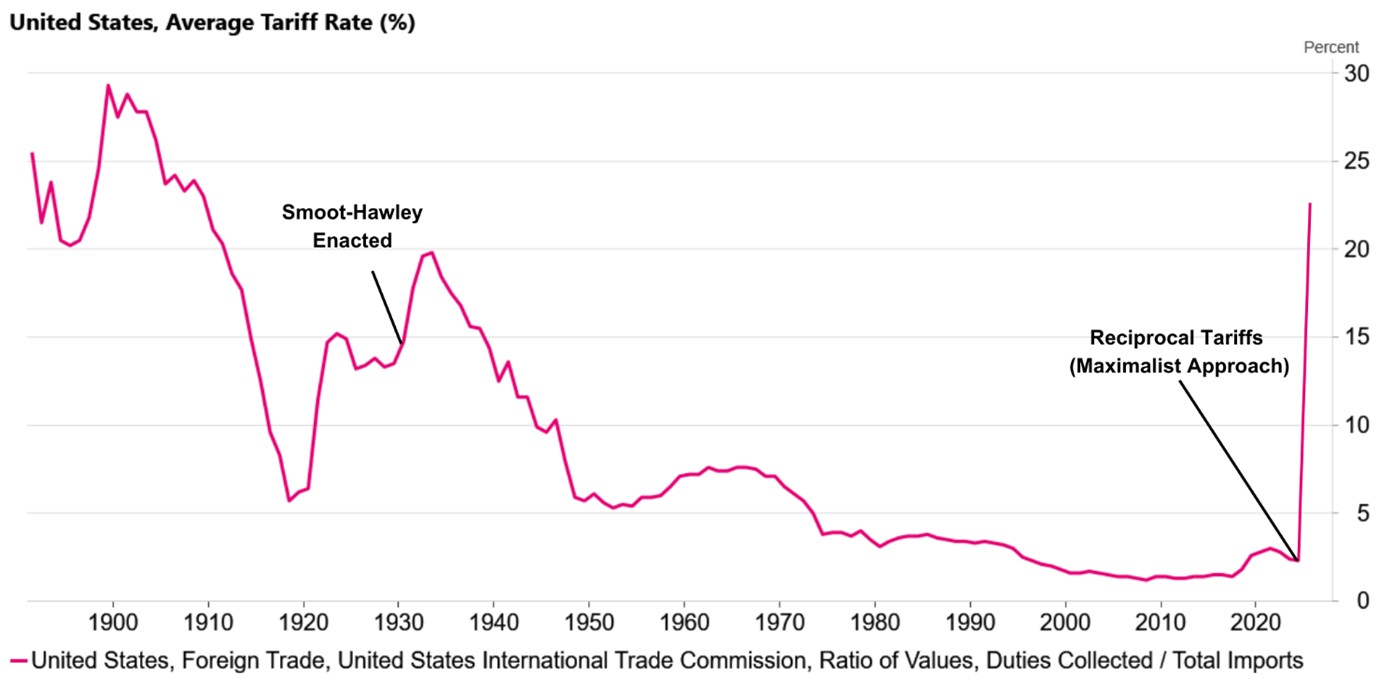

The introduction of Tariffs was not a surprise, but the magnitude was. The effective US tariff rate is now in excess of 20%. This is greater than the tariffs imposed by the US under the ill-fated ‘Smoot-Hawley’ act in 1930 and you would have to go back to the early 1900’s to see a comparable figure.

Figure 5: Effective US tariff rates (Source: US International Trade Commission, Macrobond)

At this stage it seems investors are still in reaction mode to the announcement and it will take time for markets to fully assess the impact. We’re also cognisant that this is an evolving situation, so do expect volatility (and uncertainty) to remain elevated.

At the time of writing we’ve just seen President Trump offer a 90-day pause on tariffs for countries that were willing to negotiate with the US. China’s ‘retaliation’ of an 84% tariff on US products saw its tariff rate increase to 125%. Time will tell whether these are negotiation tactics and whether the two sides will come to the table but the situation continues to be fluid.

Overall, in our view this worsens the growth and inflation mix for major economies. However the backdrop prior to the announcement has been characterised by strong earnings growth, a robust consumer and low leverage in both the consumer and private sector. It is rare that a recession is caused by government policy error, but this announcement has increased the odds of recession, whilst still not being our base case.

We appreciate this is an uncertain time for clients and such volatility can be unsettling. However, we have experienced similar volatility before and it is the nature of long-term investment that, on the path to long-term growth, periods such as this will be encountered. We are maintaining real time daily monitoring of all client portfolios. Should you have any concerns or questions, do contact your TPO Adviser.

Arrange your free initial consultation

The information in this article is correct as at 11/04/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.