Skip to main content

Skip to main content

Higher bond yields spike investor interest

In last month’s update we spoke about two prominent themes we see evolving over the course of this year. The first was regarding the diverging and contrasting growth outlook for the US compared to the rest of the world. The second relating to inflation and the challenge that Central Banks face in bringing inflation down to target and what this means for interest rate policy.

Arrange your free initial consultation

Interest Rate Cuts: A Non-Uniform Picture

Our base case would be one where we continue to see cuts in interest rates, however we do not expect this to be uniform. We’ve seen a stark revision to the outlook of interest rates with the market now pricing in just two cuts in the US compared to the six cuts that were priced in back in October. This is in contrast to the UK where weakening economic growth and uncertain outlook is likely to necessitate more rate cuts from the Bank of England.

An Unusual Trend in Yields

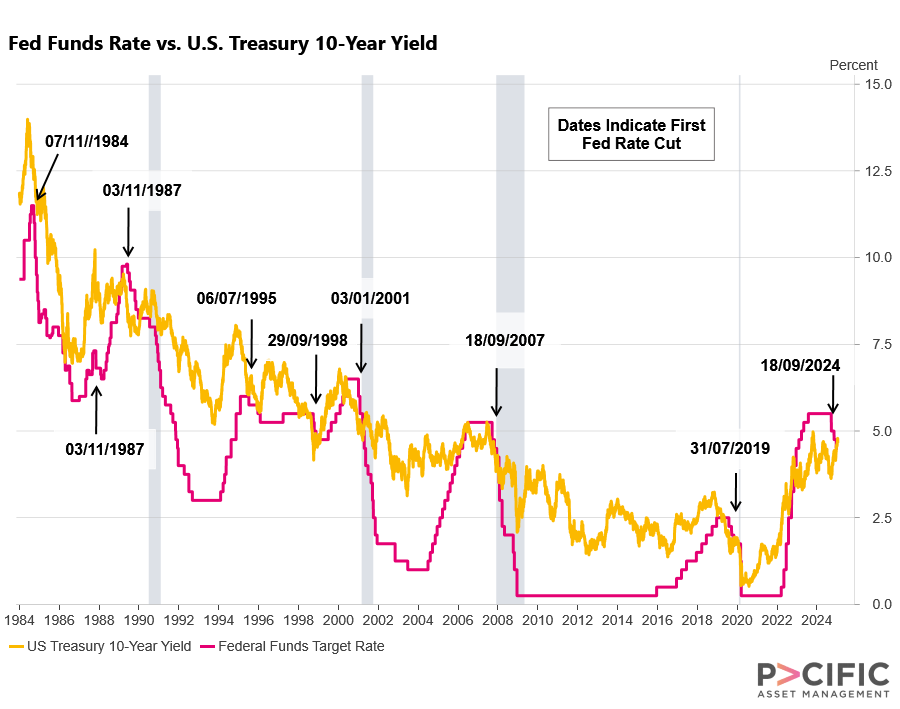

This backdrop has created a somewhat unusual occurrence where interest rates have fallen (and are expected to fall further) but long-term yields have increased (see Figure 1.).

In the US, historically, when the Federal Reserve have first cut interest rates, the 10-year yield declined causing bond prices to rise. However, since the Federal Reserve cut rates back in September, we’ve seen a marked move up in yields which has been a painful experience for investors holding longer duration (more interest rate sensitive) bonds, as their prices have fallen.

Figure 1. Fed Funds Rate vs US Treasury 10-year yield 1984-2025 (Source: Macrobond)

Figure 1. Fed Funds Rate vs US Treasury 10-year yield 1984-2025 (Source: Macrobond)

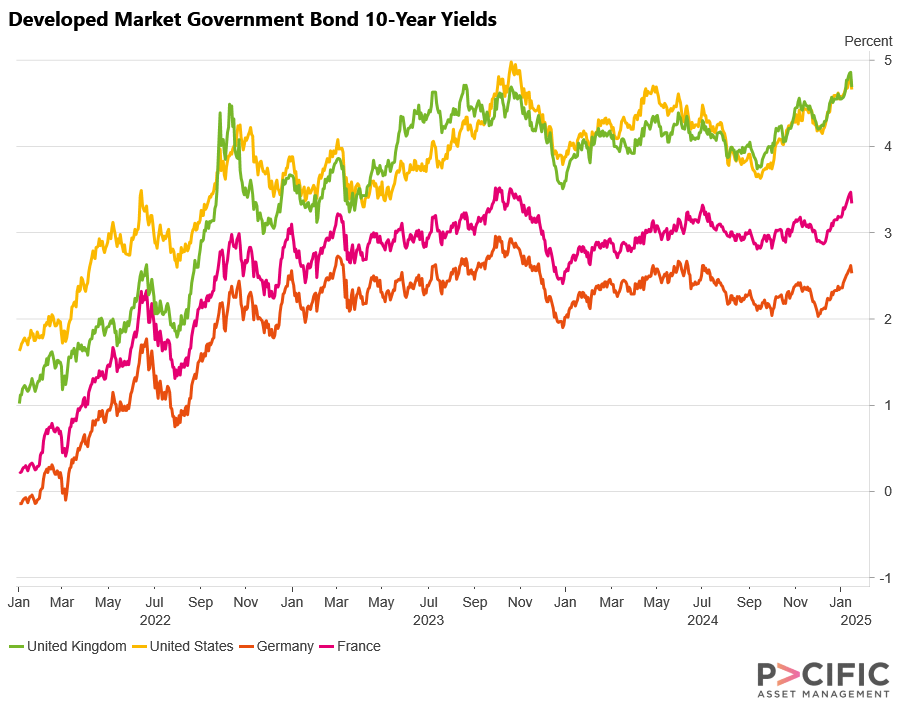

It’s important to note that this is not just a US phenomenon as we’ve seen a move up in long-term Government Bond yields in the UK and Europe as well (see Figure 2).

Figure 2. UK vs Developed Market 10-year Government Bond yields (Source: Macrobond)

Figure 2. UK vs Developed Market 10-year Government Bond yields (Source: Macrobond)

Factors Driving Higher Long-Term Yields

It has been well publicised that UK borrowing costs are now at a high not seen since 1998, however whilst there is uncertainty regarding the outlook of the UK economy there’s little to suggest at this stage there’s a broader issue in the UK Government Bond market.

Instead, the rise in long-term yields can be explained by the prospect of interest rates remaining higher for longer, concerns around inflation and the expected increase in the supply of bonds as Governments look to continue with expansionary fiscal policies.

Looking ahead we expect there to be continued volatility in yields, however with inflation falling and real yields now positive we think investors can be opportunistic in this space.

Corporate Bonds: Balancing Risks and Opportunities

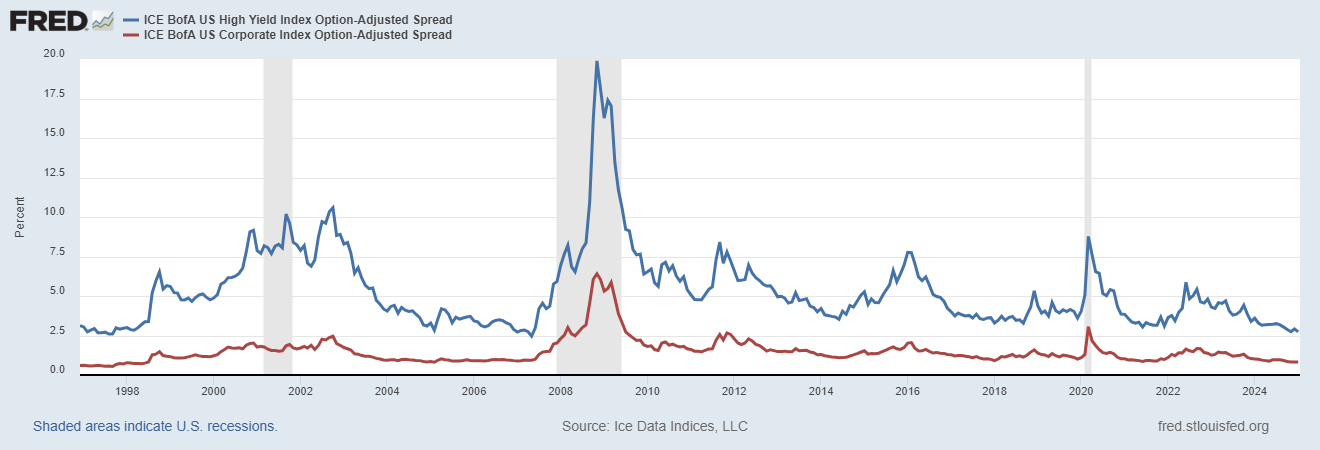

For corporate bonds the overall yield remains high but come into the year trading at a rich valuation given that the spread (the compensation one gets for investing into corporate debt) on Investment Grade and High Yield bonds are heading towards historic lows (see Figure 3.)

Figure 3. US Investment Grade and High Yield spreads (Source: FRED, January 2025)

At face value this can seem counterintuitive given the outlook for global growth which we discussed in last month’s update and the uncertainty around inflation and interest rates, which brings to mind the adage that the economy is not the market and the market is not the economy.

The absence of a hard landing, along with corporates issuing debt at low interest rates, has left them well-positioned to meet their ongoing financial obligations. We have witnessed some softening in interest coverage ratios - a measure of a company's capacity to pay its debt - in recent months, but we do not expect a significant widening in spreads given the current strength of corporate balance sheets.

Equity Valuations: Optimism or overreach?

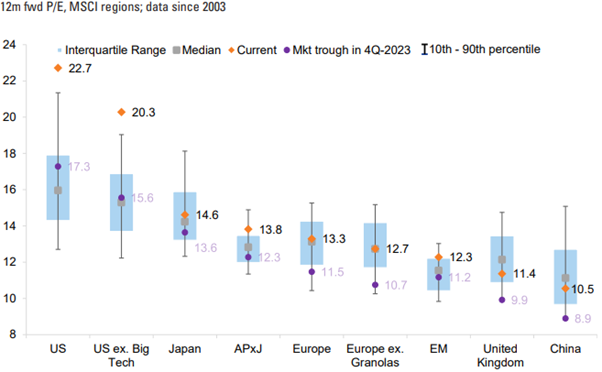

The strength of corporates has also been a contributor to a continued increase in equity valuations. Since the trough in Q4 2023 valuations have moved up across regions with the forward price-to-earnings ratio in the US now trading above its 20-year high (see Figure 4.)

Figure 4. Regional Forward Price-to-Earnings (Source: Goldman Sachs GIR)

This has seen another remarkable period for US equities and the S&P 500 has trounced the return of other regional markets. This reflecting the strength of the US economy and corporate earnings which have far exceeded their regional peers.

Conclusion

Amid volatility, investors should adopt a prudent, diversified approach, focusing on regional, sectoral, and company-specific factors. Companies with lower valuations, robust earnings, and manageable debt levels are likely to perform well over the next year. While US markets continue to dominate, global diversification could yield significant benefits as economic and earnings growth shifts across regions.

As ever, if you have any questions about navigating your personal investment environment, please don’t hesitate to contact your adviser or one of the TPO team.

Arrange your free initial consultation

The information in this article is correct as at 17/01/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.