Skip to main content

Skip to main content

MAGA uncertainty creates MEGA returns?

In our previous investment market updates, we have written about US exceptionalism i.e. the idea that the US is distinct to other countries and that this uniqueness means we should expect the US economy and stock market to continue to outperform.

This narrative, however, has been challenged in recent weeks.

Arrange your free initial consultation

President Trump's pledge to Make America Great Again (MAGA) unsettles US markets but could make Make Europe Great Again (MEGA)?

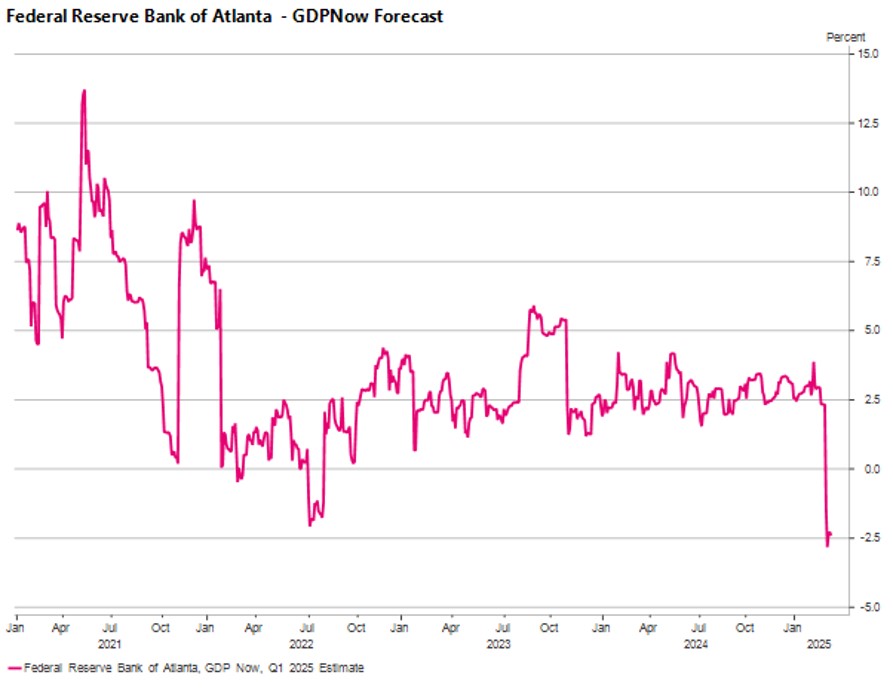

Calls that the world’s largest economy will enter a recession have grown and much has been made of the Federal Reserve Bank of Atlanta and their GDP ‘Nowcast’ model. GDP (Gross Domestic Product) is typically reported on a lagged basis every quarter, however the Atlanta Fed (as it is often referred to) look to forecast each quarter’s GDP as and when new data is released – a real time GDP model if you will - and recent readings of the model have suggested the US economy will contract nearly 2.5% on an annualised basis this quarter (see Figure 1.).

Figure 1: Sharp revision to this quarter’s GDP from the Federal Bank of Atlanta caused panic amongst investors (Source: Macrobond)

Figure 1: Sharp revision to this quarter’s GDP from the Federal Bank of Atlanta caused panic amongst investors (Source: Macrobond)

Beyond the immediate shock of the headline, on closer inspection we can see that this reading has been heavily distorted and does not reflect the true health of the US economy.

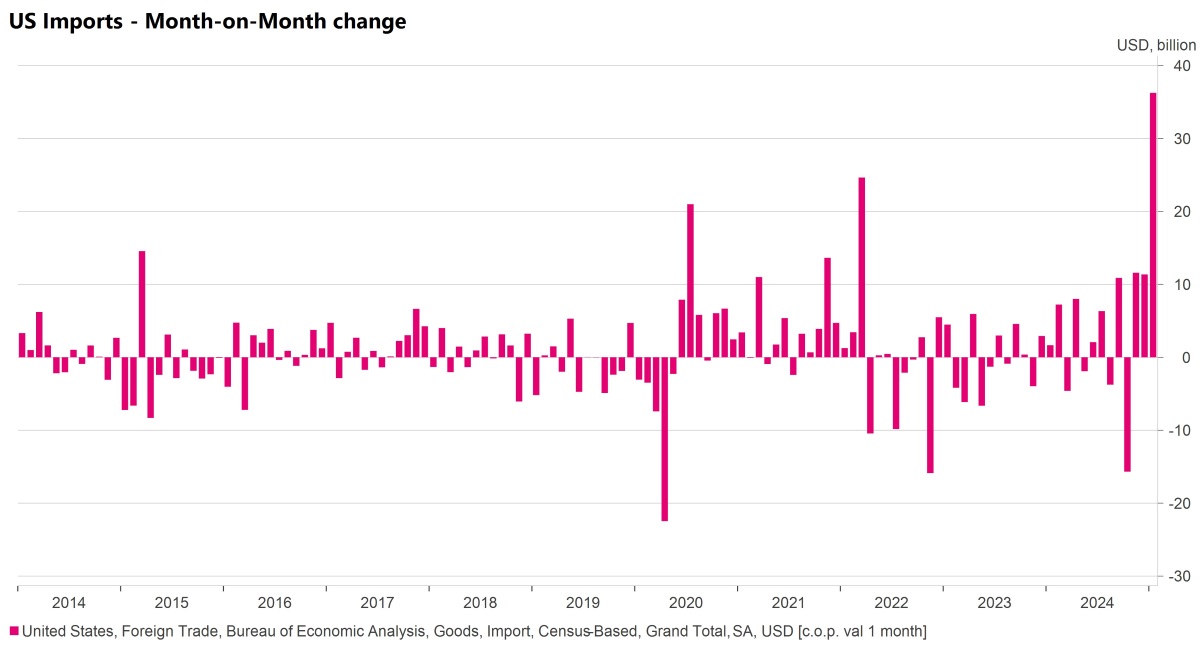

January was one of the coldest months on record in the US – the coldest January since 1988 – and this dampened consumer demand. This had a negative impact but the true distortion came from net exports falling 4% as imports jumped 13% month-on-month as businesses looked to get ahead of the impact of any potential tariffs. This was acutely seen in the import of gold into the US which contributed a large part to this increase in imports.

To put this increase in imports into context you can see the month-on-month change was greater than what we saw in the immediate aftermath of the COVID-19 pandemic and Russia’s invasion of Ukraine in February 2022 (see Figure 2.).

Figure 2: US imports increased markedly in January (Source: Macrobond)

Figure 2: US imports increased markedly in January (Source: Macrobond)

Moving forward we would not expect this to persist and we should see some normalisation in the data, however it’s still unclear whether the US economy will experience a soft or hard landing. It is our belief, at this time, that the eventual outcome will lie somewhere in the middle.

The vagueness of that statement reflects the uncertainty that we see in the US right now as only time will tell what the true impact of the Trump administration’s approach to trade policy will be and how far they will go in cuts to government expenditure.

Rather than the expectation of an impending recession, what we believe we’re seeing is investors repricing risk reflecting the increased level of uncertainty. Investors have also taken the opportunity to look beyond the US and richly valued, growth focused areas of the market to areas which are relatively cheaper and where sentiment is improving.

No region epitomises this more than Europe where an increasingly fractious relationship with the US has heralded a potential ‘sputnik’ moment with the announcement from Germany that it intends to reform its fiscal “debt brake” and spend €500bn rebuilding the country’s infrastructure.

This has helped support the momentum in economic data coming out of Europe as it continues to surprise to the upside (see Figure 3.).

Figure 3: Economic data in Europe has continued to surprise to the upside (Source: Macrobond)

Figure 3: Economic data in Europe has continued to surprise to the upside (Source: Macrobond)

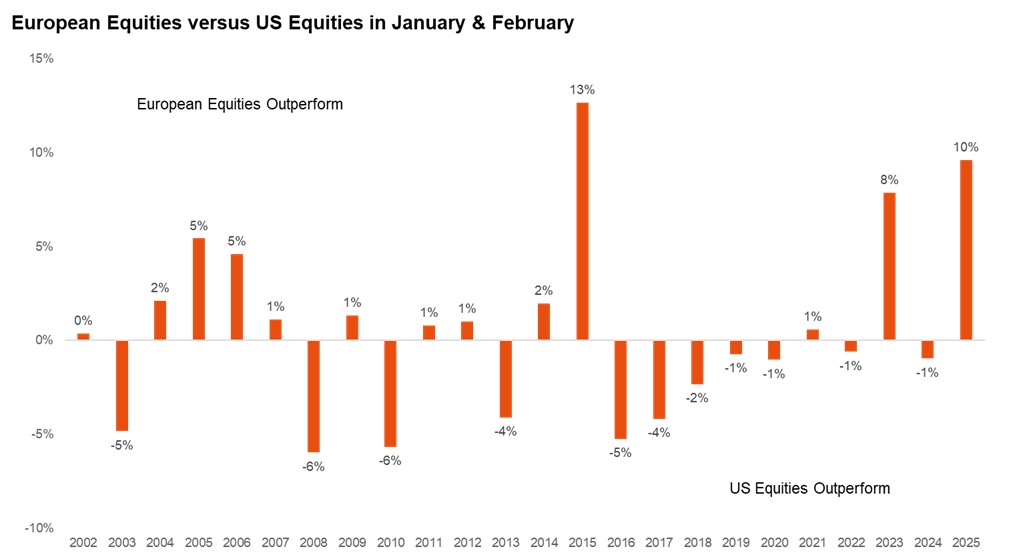

Improving sentiment and the prospect of much needed fiscal spend and investment in the region, combined with cheap valuations, has seen European equities rally year-to-date.

Over January and February, European equities have had their best start to the year relative to US equities since 2015 with the Euro Stoxx 600 outperforming the S&P 500 by nearly 10% (see Figure 4.).

Figure 4: European equities have had their best start to the year relative to US equities since 2015 (Source: Macrobond)

Figure 4: European equities have had their best start to the year relative to US equities since 2015 (Source: Macrobond)

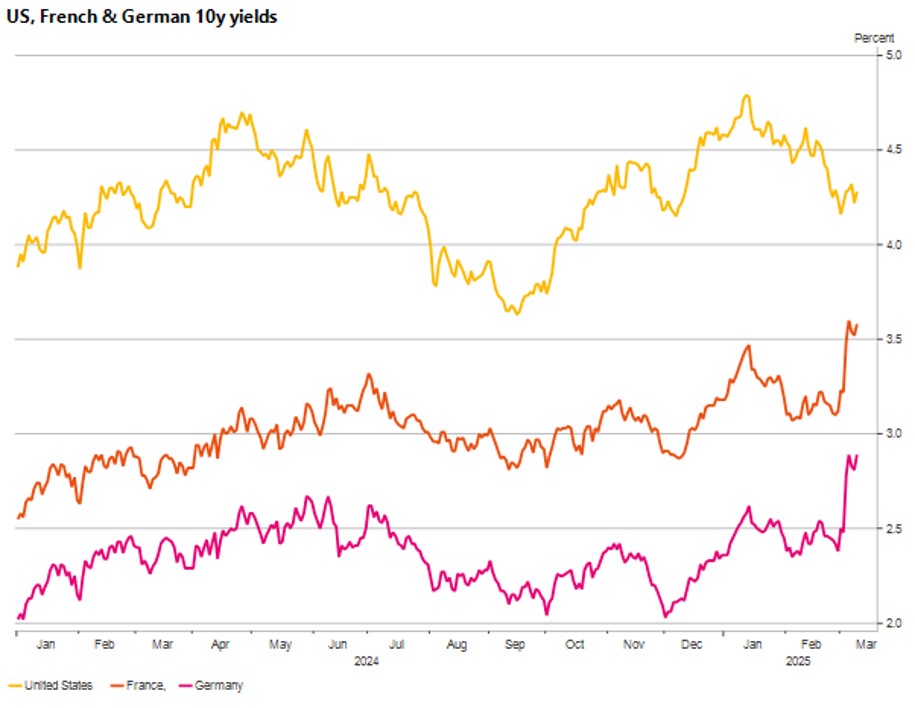

In Government Bonds we saw German 10 year yields move up 30bp in a single day which is the biggest move in the last 35 years. We also saw a move up in broader European Government Bond yields on the prospect of further borrowing (and spending).

Notably we didn’t see the same move in US Government Bonds which is unusual given the historic close correlation, but again this illustrates the diverging paths of the respective economies and fiscal policy (see Figure 5.).

Figure 5: Economic data in Europe has continued to surprise to the upside (Source: Macrobond)

Figure 5: Economic data in Europe has continued to surprise to the upside (Source: Macrobond)

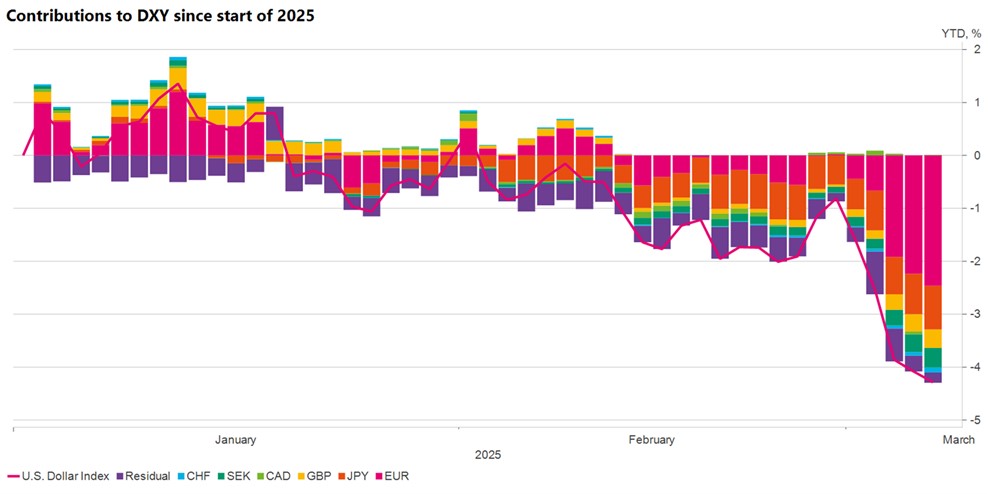

Volatility in markets was not just confined to equities and bonds. Since the start of the year we’ve seen the US Dollar weaken against major currencies. Looking at the DXY Index which measures the strength of the US Dollar against a basket of major foreign currencies, it is down 4% year-to date (see Figure 6.).

This can seem counterintuitive given that tariffs from the US were considered Dollar positive, however the market is now reassessing the impact of tariffs and the negative growth shock this could have on the US.

Figure 6: The US Dollar has weakened against major foreign currencies since the start of the year (Source: Macrobond)

Figure 6: The US Dollar has weakened against major foreign currencies since the start of the year (Source: Macrobond)

Given the current fast moving nature of markets , there’s a possibility that this note will already be out of date by the time that you read it. You’d be forgiven for wondering how today’s or this week’s latest headline will impact your investments.

We understand that uncertainty can be uncomfortable but what we also believe is that uncertainty can become an opportunity assuming one has the right tools. For multi-asset investors, this period of heightened volatility presents the chance to manage risk more effectively and generate returns from different areas, as a broader range of market winners and losers emerge.

As ever, if you have any questions or concerns, please get in contact with your TPO Adviser who can explain how we’re actively managing assets and portfolios to minimise this period of volatility.

Arrange your free initial consultation

The information in this article is correct as at 14/03/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.