Skip to main content

Skip to main content

Technology turbulence and regional gains

After a pullback in December 2024, we saw global equities resume their move upwards as the MSCI World index returned 3% in January 2025. However, as we discussed recently, investors should be prepared for volatility and we saw a brief but volatile episode towards the end of the month with the emergence of DeepSeek.

Arrange your free initial consultation

DeepSeek, AI and Technology Stocks

DeepSeek – a Chinese AI company – has developed an AI model which reportedly has comparable quality to OpenAI (a US AI company) but at a fraction of the cost. Initial estimates are that DeepSeek spent just $6m dollars developing the model compared to the $5bn that OpenAI is expected to spend this year.

This came as a surprise to investors as export controls have limited the sale of Nvidia’s high powered Graphic Processing Units (GPU’s) to Chinese companies. As a result investors have begun to question the return that will be made on the vast amounts of capital that US technology companies have invested into AI projects.

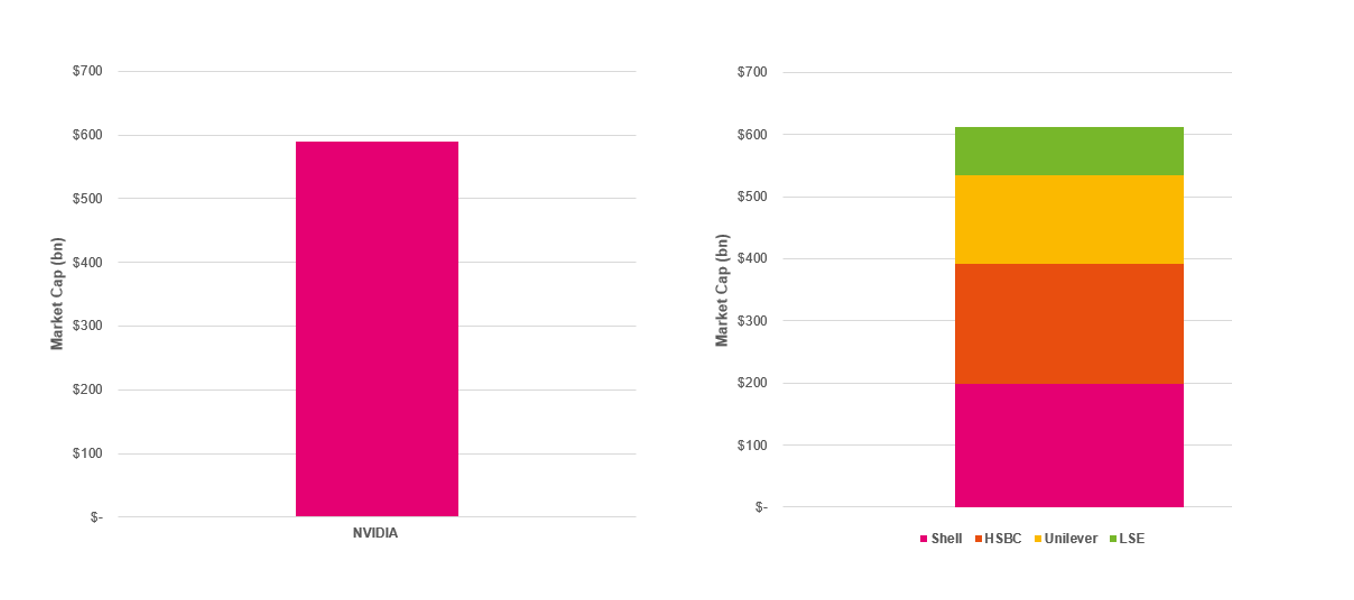

Following this announcement we saw Nvidia post the largest drawdown in US history with the company falling 17% on the news, which was a $600bn loss in market capitalisation. To put this into context, $600bn is the entire market capitalisation of Shell, HSBC, Unilever and the London Stock Exchange (see Figure 1).

Figure 1. The fall in Nvidia’s share price was the equivalent to the market capitalisation of four UK equity market stalwarts (Source: TradingView)

Whilst Nvidia fell we saw Chinese Technology companies rally on the news as investors began to reappraise the outlook for the sector and begin to question the dominance of US technology companies.

The Hang Seng Tech index which is a composite of the 30 largest technology companies listed in Hong Kong and includes companies like Alibaba, JD.com and Tencent, rallied 3% on the day and finished the month 12% up. This compares to the US tech centric NASDAQ index which returned just 2.7% over the same time period.

Figure 2. Chinese technology companies rallied on the news of DeepSeek (Source: Pacific Asset Management)

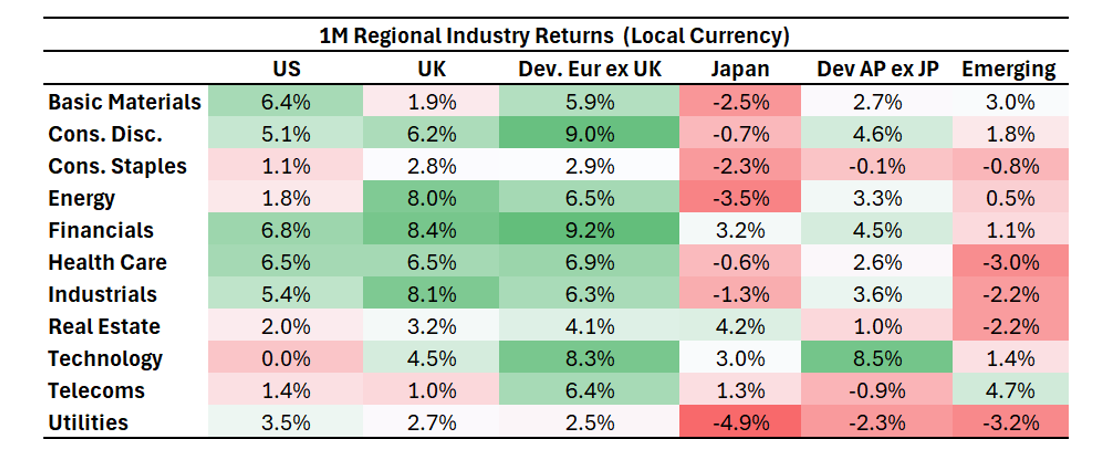

We also observed a broader rotation within the US as the S&P 500 equal weight index – an index where each company has the same weight (0.20%) – outperformed the S&P 500 which has a 35% allocation to just seven (‘Magnificent’) stocks.

Part of this is due to the composition of the equal weight index which has less exposure to technology companies (a 13% allocation compared to the 36% allocation in the S&P 500) and a larger allocation to industrials and healthcare both of which outperformed technology last month (see Figure 3).

Figure 3. Returns of regional industry sectors (Source: FTSE Russell)

Regional Returns and Sector Rotation

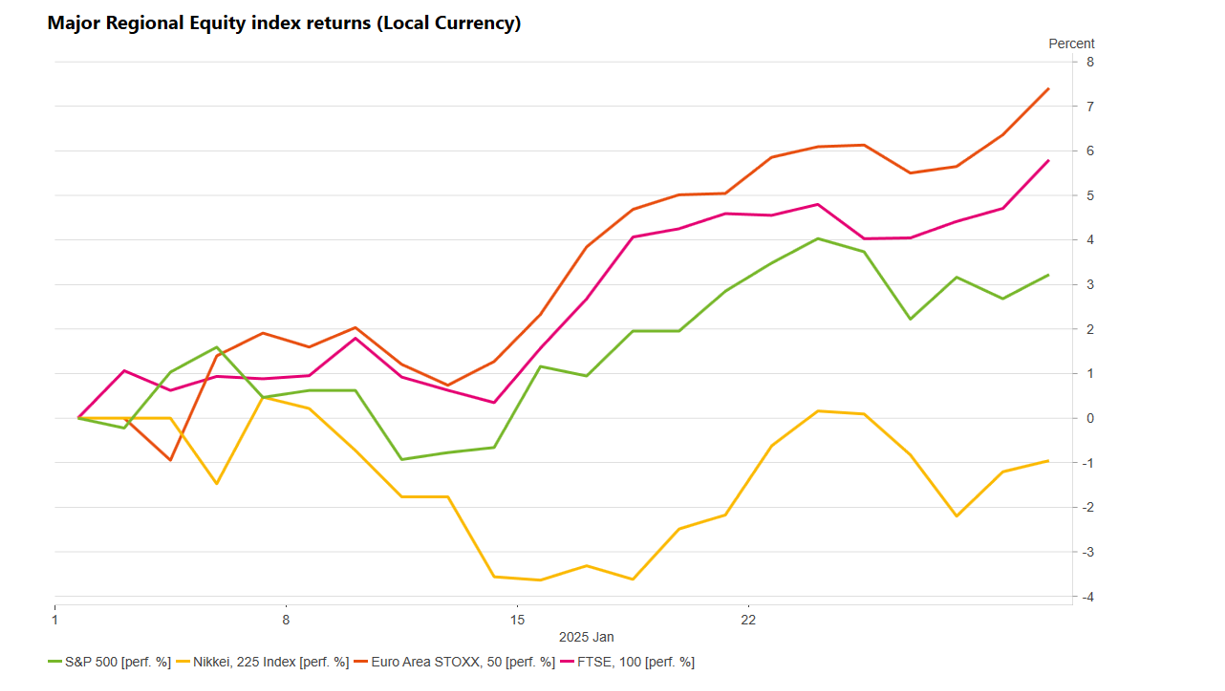

In a rare showing we saw both European and UK equities outperform US equities last month.

Economic growth in Europe continues to be modest. However, an improvement in business activity and ECB interest rates cuts have provided a supportive backdrop for European equities with the Euro Stoxx index up 7.9% last month.

In the UK and Japan we saw moves in the respective countries currency drive equity returns. A weakening pound sterling supported UK equities given that 75% of the revenue generated by companies listed on the FTSE 100 is earned overseas, a weakening pound increases the value of overseas earnings. Meanwhile in Japan we continue to see strong wage growth and the Bank of Japan have indicated that there will be further rate increases which saw the Yen rally against the Dollar. This weighed on the export focused Japanese equity market as Japanese exports became relatively more expensive due to relative Yen appreciation.

Figure 4. Returns of regional equity indices (Source: Macrobond)

Figure 4. Returns of regional equity indices (Source: Macrobond)

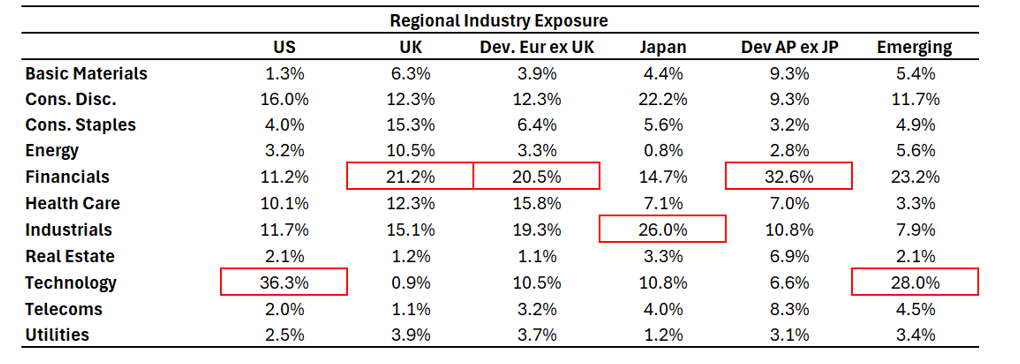

Another important consideration for investors is the industry exposure of regional equity markets.

One reason why the US equity market has been so dominant in recent years is due to the index’s exposure to technology companies. Around 36% of the S&P 500 is in technology companies compared to less than 1% in the FTSE 100.

By comparison the UK equity market can be described as the ‘old economy’ with a larger allocation to Industrials such as Financials and Energy. Similarly in Europe there is a larger allocation to Industrials and Healthcare and again a relative underweight to Technology (see Figure 5).

Figure 5. Regional industry exposure (Source: FTSE Russell)

Figure 5. Regional industry exposure (Source: FTSE Russell)

Given the noise in financial markets it can be useful to step back and reassess where we are or what prevailing narratives are on the mind of investors. One of these is the exceptionalism of the US economy (and equity market) and whether this will continue.

We retain a positive outlook for the US given the robustness of the economy and relative strength of US corporates, however we’re mindful that no individual country continuously outperforms.

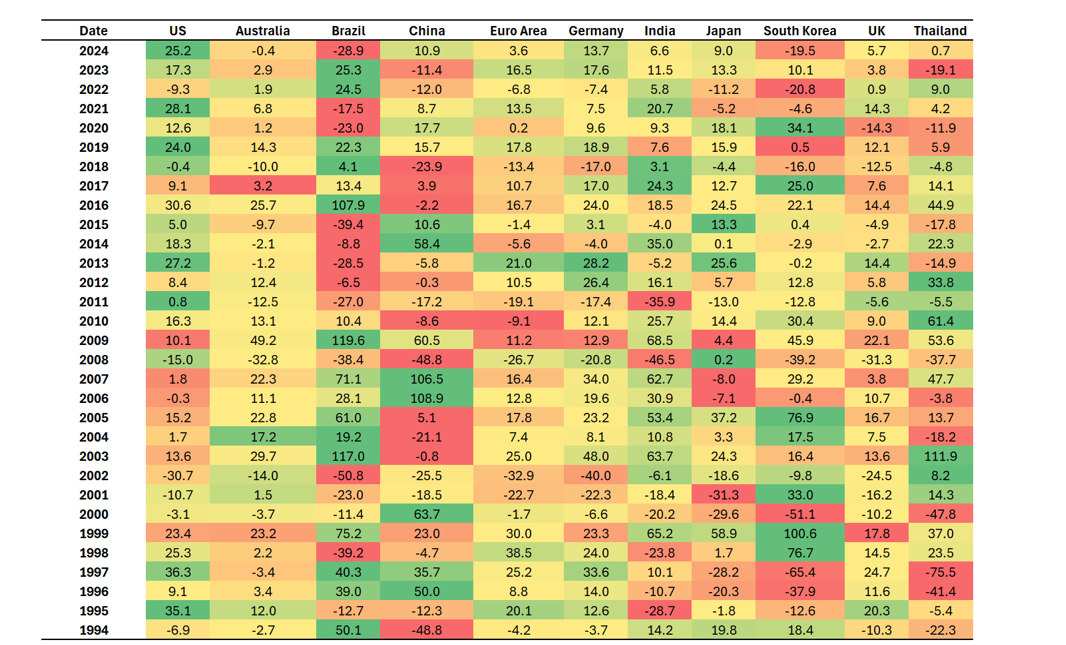

You can see this when we look at the returns of various equity markets over the last thirty years. It also highlights the potential opportunity that investors have by looking beyond the US and being proactively tactical with their investments (see Figure 6).

Figure 6. Historic equity returns (in sterling) have varied significantly over the last 30 years (Source: Macrobond)

Conclusion

Last month was another example of the benefits of having a diversified portfolio.

Increased volatility in markets typically creates opportunities to buy assets at more attractive valuations or take advantage of short-term trends. By being proactive investors can strategically adjust their allocations to asset classes, regions and sectors to not just reduce overall risk but also potentially improve total returns.

As ever, if you have any questions about navigating your personal investment environment, please don’t hesitate to contact your adviser or one of the TPO team.

Arrange your free initial consultation

The information in this article is correct as at 14/02/2025.

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions. Investment returns are not guaranteed, and you may get back less than originally invested; past performance is not a guide to future returns.