Skip to main content

Skip to main content

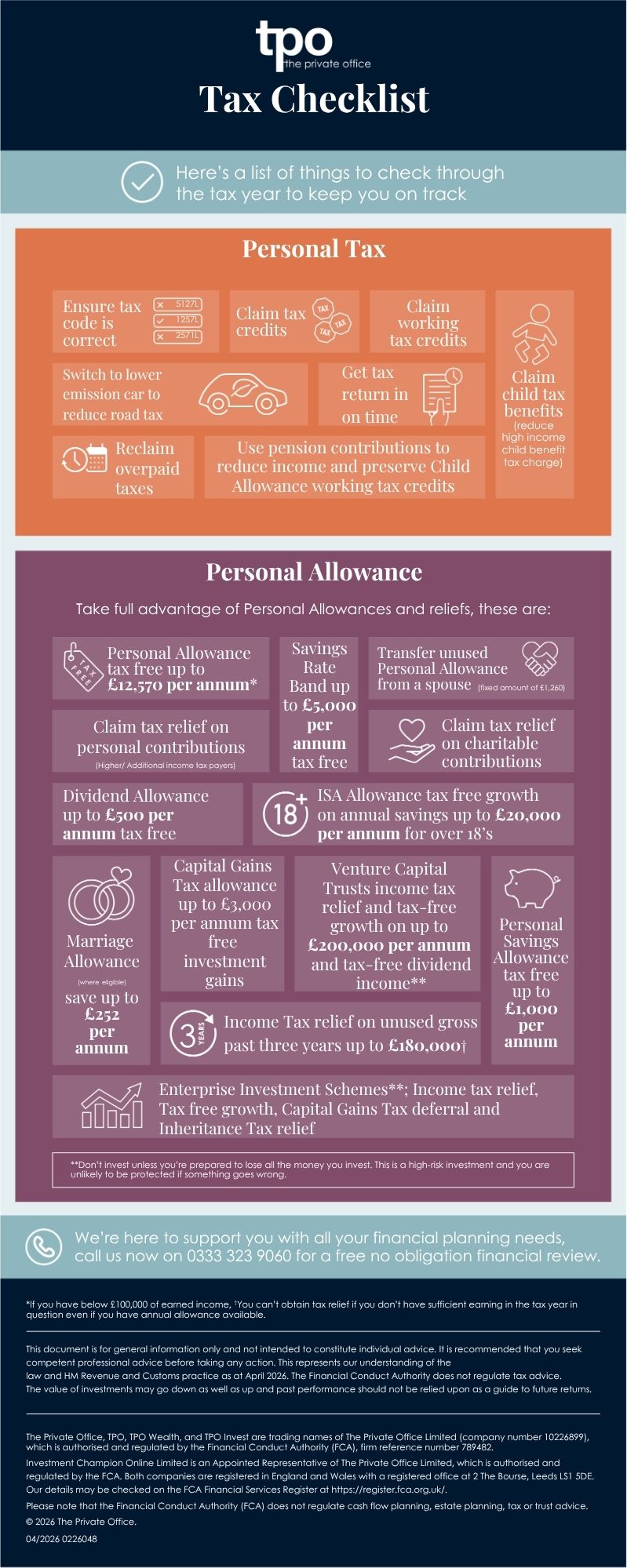

Personal Tax and Allowance Checklist

With data from the LCP partner, Steve Webb (former Pensions minister), showing there may be 2.5 million new higher rate tax (HRT) taxpayers due to freezes in tax thresholds, now - more than ever - it's important to know your personal taxes, allowances and reliefs.

Here we list out some tips on keeping track of important things during the tax year, with suggestions on how to make the most of your personal allowances and tax credits.

Have you checked your tax code?

Checking your tax code is important because it ensures that you're paying the correct amount of tax. Your tax code determines how much tax should be deducted from your income by your employer or pension provider. If your tax code is incorrect, you could end up paying too much tax and missing out on money you're entitled to, or you might pay too little and face a tax bill later down the line.

According to the BBC, potentially millions of Brits are using the wrong tax code, which begs the question; how often should I check my tax code? Ideally, you should regularly check your tax code for any potentially changes, most importantly checking following a change in job, income, and marital status.

What if I am on the wrong tax code?

If you are on the wrong tax code, please click here. Thankfully, once you have updated your information with HMRC, HMRC will automatically update you to the relevant tax code and automatically repay any overpaid taxes.

If you have started a new job, you may have been placed on an emergency tax code. Once your employee has updated HMRC, you will automatically be issued a refund for any excess tax paid.

Please see the deadlines below for reclaiming tax:

- Tax year 2022/23 claim by 5 April 2027

- Tax year 2023/24 claim by 5 April 2028

- Tax year 2024/25 claim by 5 April 2029

- Tax year 2025/26 claim by 5 April 2030

- Tax year 2026/27 claim by 5 April 2031

Have you claimed your Tax credits?

Every year, you should check for tax credits because the eligibility and amounts of these credits vary depending on your income, the size of your family, and your personal circumstances. By checking your eligibility for tax credits each year, you ensure you're getting all the credits you qualify for and make the most of your tax benefits. Furthermore, as tax laws and regulations are subject to change every year, you might not be eligible for the same benefits that you were in the previous tax year. By checking your tax credits on a regular basis, you can stay on top of any changes and make sure you're utilising all the opportunities to lower your tax bill and improve your financial situation.

Child Benefit is available for those responsible for raising a child under 16, or under 20 if they're in approved education or training. Only one person can claim for each child, with rates varying from £27.05 weekly for the eldest or only child to £17.90 per additional child.

You may be eligible for Universal Credit. From 6th April 2026 the standard rate of Universal Credit will increase to the following amounts, depending on your personal circumstances:

- If you’re single and under 25 = £338.58 per month

- If you’re single and 25 or over = £424.90 per month

- If you’re in a couple and are both under 25 = £528.34 per month

- If you’re in a couple and one or both of you are 25 or over = £666.97 per month

Are you maximising your personal allowances?

Use our handy check list to ensure you're making the most of them.

To optimize tax efficiency, individuals can take advantage of various allowances and reliefs. One basic benefit is the Personal Allowance, which offers a tax-free level of up to £12,750 annually. Pairing this with the Individual Savings Account (ISA) Allowance allows for tax-free growth on savings of up to £20,000 annually for those over 18.

A variety of allowances offer ways to generate revenue that is tax-free. Eligible couples can take advantage of the Marriage Allowance which lets you transfer £1,260 of your Personal Allowance to your husband, wife or civil partner (subject to other income received). This reduces their tax burden by up to £252 each tax year. Furthermore, dividend income up to £500 per year is tax-free under the Dividend Allowance, and savings up to £5,000 per year is tax free under the Savings Rate Band (subject to other income received). In addition, people can receive tax-free interest income of up to £1,000 annually thanks to the Personal Savings Allowance, which improves their total financial flexibility.

There are more tax relief options outside basic allowances. Contributions to charities are tax deductible for individuals, which lowers taxable income and promotes charitable activities. Tax relief on personal contributions is another benefit for taxpayers with higher or additional incomes, which helps them save more for retirement. Furthermore, individuals can receive Income Tax relief on unused gross pension contributions from the past three years, up to a maximum of £160,000 (subject to conditions).

Venture Capital Trusts (VCTs) and Enterprise Investment Schemes (EIS) are UK investment options that offer significant tax relief benefits, appealing to individuals seeking to reduce their tax bills while supporting small, high-risk companies. Investing in a VCT can provide up to 20% income tax relief on investments up to £200,000 per year, provided the shares are held for a minimum of five years. Additionally, any dividends received from a VCT are tax-free. EIS offers similar tax relief, with up to 30% relief on investments up to £1 million annually (or £2 million if investing in knowledge-intensive businesses), plus potential exemption from Capital Gains Tax and Inheritance Tax under certain conditions.

However, there are risks and downsides to consider. Both VCTs and EIS invest in small and potentially unstable companies, presenting a higher risk of loss compared to more traditional investments. These schemes are also less liquid, meaning it can be challenging to sell shares quickly. Due to the complexity of these investments and their tax implications, it's often advisable for investors to consult with financial advisers to fully understand the benefits and potential pitfalls.

Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment and you are unlikely to be protected if something goes wrong. |

|---|

If you would like to know more about how we can help you with tax year end, contact us to speak with an expert adviser.

Arrange a free initial consultation

The Financial Conduct Authority does not regulate tax advice.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Past performance is not a guide to future returns.

Investment returns are not guaranteed, and you may get back less than you originally invested.