Skip to main content

Skip to main content

The Great Wealth Transfer: an opportunity for HMRC

The United Kingdom is set to witness an unprecedented shift in financial assets and wealth in what is being labelled as the “great wealth transfer.” ‘Baby boomers’ (born between 1945-1965), who collectively hold a significant portion of the nation's wealth, are poised to pass down £5.5 trillion over the next two decades.

Generational Windfall: The Great Wealth Transfer

Whilst the expedited timescale of the passing down of capital and assets represents an extraordinary opportunity for younger generations to accumulate wealth, there is also the potential for significant financial challenges for families across the UK set to inherit these estates. These could range from stress and anxiety of receiving large sums of money someone has not managed before, through to fast changing tax policy leaving estates previously unaffected by Inheritance Tax (IHT), suddenly facing a large liability.

Arrange your free initial consultation

Labour’s Autumn Budget and Its Impact

Labour’s recent Autumn Budget has added a layer of urgency to IHT planning. Among the numerous changes announced, the most significant include extending the freeze on IHT thresholds until 2030, bringing inherited pensions into the taxable estate from April 2027, and diminishing Agricultural Property Relief (APR) and Business Property Relief (BPR) changes from April 2026, which will mean that agricultural assets over £1,000,000 will face a 20% tax bill, pushing many into selling land off.

The IHT threshold freeze keeps the nil-rate band at £325,000, a figure unchanged since 2009, despite the ever-present effects of inflation reducing the real value of this over the years, historically soaring house prices , and now the inclusion of pensions into the estate. This could be seen to be yet another form of ‘fiscal drag’ or stealth tax, pinching individuals and families with the country paying the highest levels of tax in 70 years, and HMRC collecting 37% of the UK’s total GDP in tax receipts.

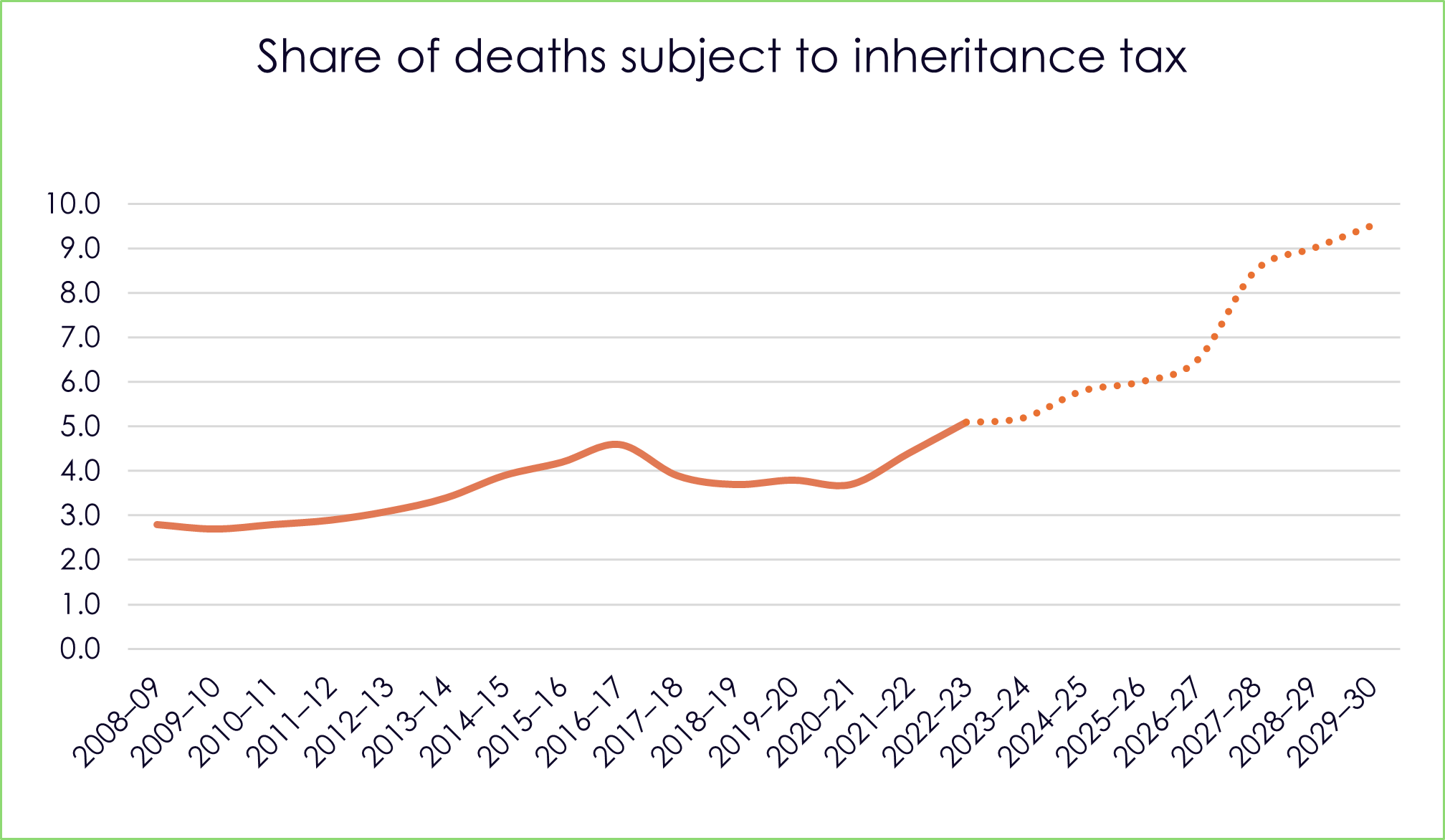

Figure 1 - Share of deaths subject to Inheritance tax, Source: IFS Report R235, 2022

For many families, this means that wealth once thought safe from IHT may now face the 40% levy. Rising property values, especially in the South East, push even modest estates above the threshold, leaving fewer households exempt. With Labour’s changes expected to swell government IHT receipts even further—already up 11% year-on-year. Between 2024-25 and 2028-29, the OBR now estimates the Treasury will collect more than £50bn in inheritance tax alone, a 19% increase of more than £8bn compared to the forecast made following ex-chancellor Jeremy Hunt’s Spring Budget in March 2024. Navigating this shifting tax landscape will be critical for those looking to preserve their legacy and look after their children once they are gone. When an estate is liable to IHT, the average amount paid stood at £215,000 in the Tax Year 2021-22, and the future forecasts only point in one direction, which is up.

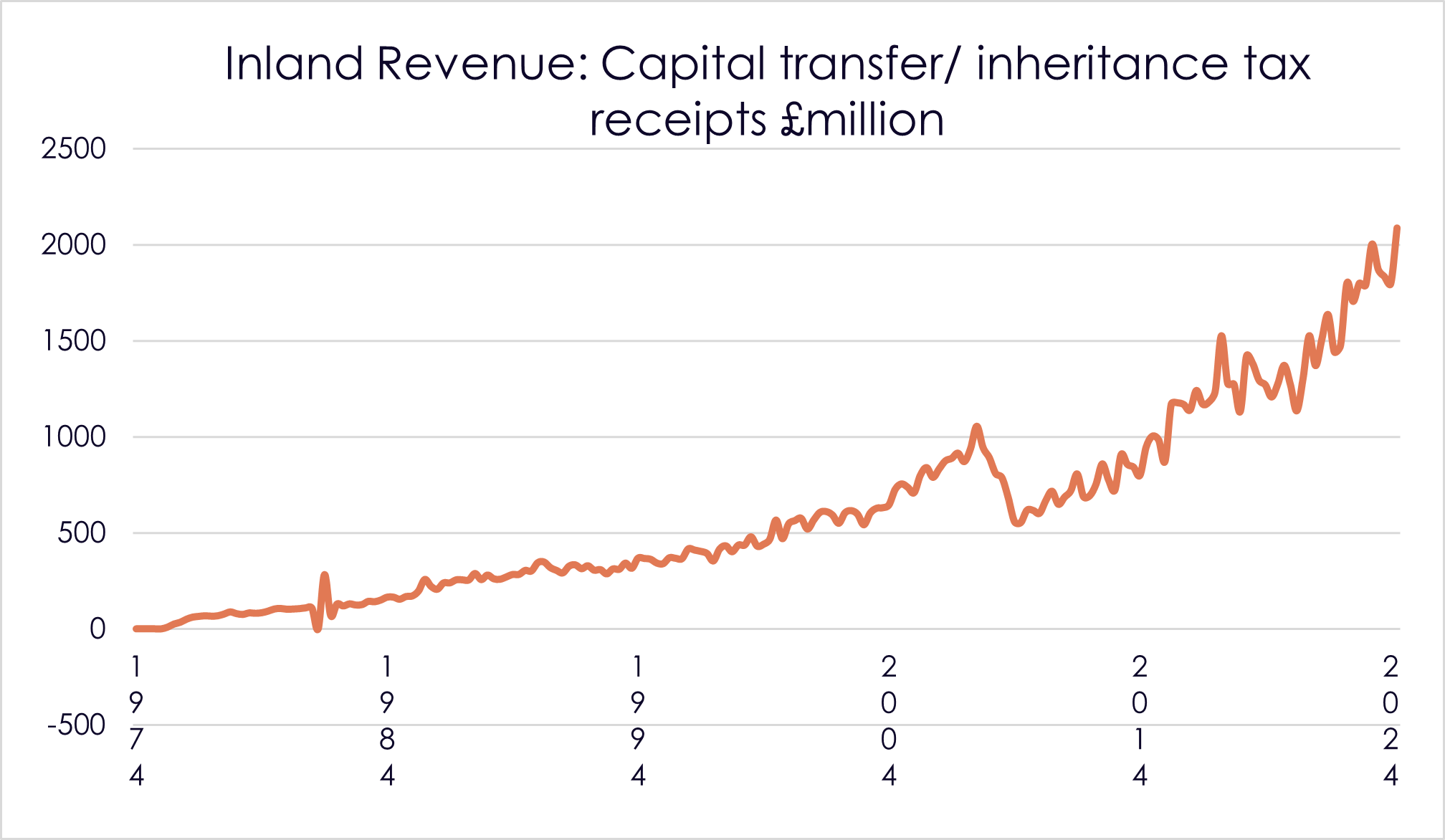

Figure 2 - Inland Revenue: Capital transfer/ Inheritance tax receipts £million, Source: Office for National Statistics, 2024

Opportunities and Challenges of the Wealth Transfer

This generational windfall presents a double-edged sword. On one hand, it could offer younger generations the financial support needed to tackle rising living costs, fund housing purchases, or build a secure retirement. On the other, without professional advice, much of this wealth could erode before it can deliver meaningful benefits. Giving too much too soon could leave aging parents without the resources to fund long-term care, and poorly structured plans can further lead to significant tax bills, family disputes, or mismanaged assets . Due to the complexities of managing large estates and recent changes, it is more essential than ever before for families to plan proactively.

Preparing for the Transfer

For those expecting to receive or pass on wealth, there are several practical steps to mitigate tax exposure and ensure financial security:

- Gifting Strategically: Taking advantage of the £3,000 annual gifting allowance or larger tax-free gifts during life can reduce the taxable value of an estate.

- 7-year rule: If you die within 7 years of gifting an asset to an individual, the 7-year gift rule in inheritance tax means that the beneficiary may be required to pay IHT. If you survive 7 years, then the gift may be IHT free.

- Consider Life Assurance: Whole of life cover is not designed to stop IHT outright, but rather to assist beneficiaries of the estate to meet the liability in the form of a lump sum on the death of the policyholder. It is crucial to get professional advice on this to help calculate the size of the estate, the amount of tax that could be due, and therefore size of the lump sum required on death and the cost of premiums this could result in.

- Cash flow planning: helps illustrate information regarding how much of an estate someone can gift away without causing unnecessary detriment to their own lifestyle and ability to fund potential long-term care should it be needed.

- Setting Up Trusts: Trusts provide a way to transfer wealth while maintaining control and reducing tax liabilities.

- Seeking Professional Advice: A financial adviser can help families structure their estates to align with personal goals and minimise tax exposure.

Why Act Now?

Labour’s Budget changes demonstrate the rules governing inheritance and taxation are in constant flux. Early planning is critical to ensure that your hard-earned wealth benefits those you care about most, rather than being diminished by unnecessary tax bills. Whether you are planning to pass on your estate or a beneficiary preparing for an inheritance, acting today could hopefully safeguard your family's financial legacy for generations to come.

If you’re concerned about IHT on your estate and want to learn, why not get in touch for a free initial consultation.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, tax, or trust advice.

![]()