Skip to main content

Skip to main content

Pensions vs Property - which is best?

A popular question often asked by clients is whether they should contribute into a pension or invest in a property portfolio to fund their retirement.

The reality is there are pros and cons for each investment vehicle, so it’s important to look at these along with how returns compare over the last 10 years. Here we break these down so you can better understand which option may be better suited for you. Although we would always recommend speaking to a financial expert before embarking on your decision.

Arrange your free initial consultation

Pension

Advantages

- Personal pension contributions attract income tax relief at your marginal rate. This means for basic-rate taxpayers, a £1 contribution essentially costs you 80p, as 20% tax relief is provided by the Government under the ‘relief at source method’. Your contributions can also help you reclaim certain tax allowances, such as the personal allowance, tax-free childcare, and child benefit entitlement. If you’re a higher rate taxpayer, you can claim an additional 20% or even 25% tax relief for an additional rate taxpayer.

- Employer pension contributions are essentially ‘free money’ as your employer is providing this as an additional benefit in your remuneration package – often if you don’t take up the contributions, they won’t provide an alternative income instead. Business owners can reduce their Corporation Tax liability by making contributions into their own name.

- Any investment growth is free of Income Tax and Capital Gains Tax.

- Usually, 25% of the value can be withdrawn tax-free in retirement.

- Ability to invest in a diversified range of asset classes (cash, fixed interest, shares, property, and other instruments). Further diversification can be achieved by diversifying assets geographically.

- Flexibility to draw an income in retirement through various methods such as a Lifetime Annuity, Fixed-Term Annuity, and Flexi-Access Drawdown.

- If structured appropriately, any remaining funds after your death can sit outside of your estate for Inheritance Tax (IHT) purposes. This can be a tax-efficient way of passing wealth on between different generations.

Disadvantages

- You are unable to access your pension funds until age 55. This will be increased to age 57 from 6 April 2028.

- The value of your pension is subject to investment risk.

- Depending on how much you spend and how long you live for, your pension pot could be exhausted during retirement if not managed appropriately.

- Legislation can be complex, and rules are often changed.

- On-going charges will apply (pension provider/platform, investment related charges and financial adviser fees).

Property

Advantages

- Potential for long-term capital appreciation and an opportunity of outperforming inflation over the long-term.

- Potential for a regular rental income stream. This can provide a consistent cashflow which can be reinvested into property or other assets.

- A diversifying asset as part of an overall investment portfolio, which means that it can provide a hedge against market volatility.

- Property improvements can add to the value and/or increase rental yields.

- Physical asset and you own something tangible.

- 20% tax-credit available on mortgage interest.

Disadvantages

- If capital is required, it can often be a lengthy process to release equity.

- High initial costs (legal fees and stamp duty etc). A surcharge of 3% on top of normal stamp duty rates applies on purchase of an additional property.

- Potential debt if you require a mortgage to fund the purchase.

- Property management. This can be a hassle, stressful, and time consuming. Paying a professional will eat into your rental yield.

- Maintenance – any repairs will need to be carried out swiftly and the costs are funded by you.

- Potential void periods. This can be a tricky situation to find yourself in if you have a buy-to-let mortgage.

- Tax credit on mortgage interest restricted to 20%, even if you are a higher-rate or additional-rate taxpayer.

- Capital Gains Tax will be applied on any profit when sold.

- Included as part of your estate for IHT if held until you pass.

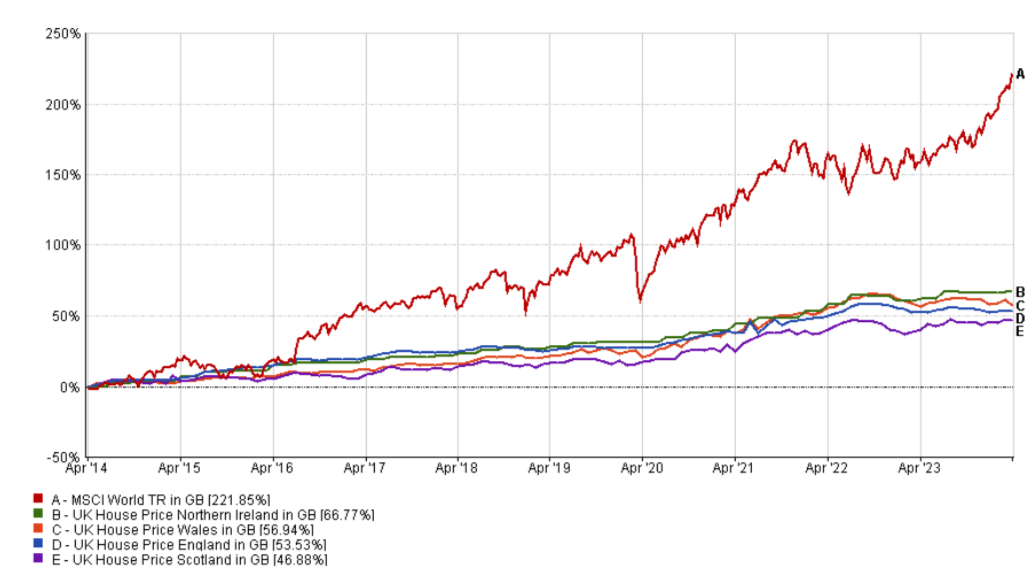

Pension vs Property Performance

A common issue UK property investors face is that the value of their portfolio is influenced by the UK economy and sentiment.

Investing through a pension can be a much simpler way to diversify globally and across different asset classes through a basket of funds. This can help smooth out governmental decisions or country specific issues, and benefit from growth in other economies.

Past performance is not a reliable indicator of future performance.

Figure 1: Stock market performance VS Property - Source: FE Analytics, 2024.

The chart above demonstrates the stock market has outperformed UK property over a 10-year period.

The MSCI World Index measures the performance of equity markets across developed countries and has returned 221.85% over this period. UK property returns range between 46.88% - 66.77%.

However, it is important to note these property returns are based on capital appreciation only and do not include any rental incomes received. According to NatWest, as of 2024, the average annual UK rental yield is between 5% and 8% gross.

Should I invest in property or a pension?

Both investment vehicles provide different advantages and disadvantages, as detailed above, and each have a place within a diversified portfolio. As each of our personal circumstances can vary widely, is important to seek advice. An independent financial planner will be able to help you establish which solution is most suitable for your own personal needs. If you’d like to speak to one of our expert advisers, why not get in touch for a free initial consultation, to see if we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate estate planning, tax advice or most types of buy-to-let mortgages.

Your property may be repossessed if you do not keep up repayments on your mortgage.

Investment returns are not guaranteed, and you may get back less than you originally invested.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available. Your pension income could also be affected by the interest rates at the time you take your benefits.

The information contained within this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.