Skip to main content

Skip to main content

How certain are your retirement plans?

It is fair to say, the last seven years or so have brought multiple periods of market uncertainty. It feels relevant to reference 2018, the year of Trump vs China’s trade war which has once again reared its ugly head in 2025 with Trump’s ‘liberation day’ and the uncertainty that has brought to investment markets. Outside of these events we have had a pandemic, multiple geo-political conflicts, and a lengthy period of increased inflation whereby central banks around the world had no choice but to raise interest rates in an attempt to curb and reduce inflation over time. In some regions the rhetoric had been ‘higher interest rates for longer.

With the above in mind, it feels more important than ever for clients to have an understanding of the financial track they are on and where this is headed. Our existing clients will know that what serves as the foundation of this understanding is cash flow forecasting. This is such an essential tool in ensuring your wealth is segmented in such a way that enables you to make sure that the risk associated with investment markets can be managed as best as possible.

Arrange your free initial consultation

Have your retirement plans been derailed?

For those not fortunate enough to have a guaranteed, and usually inflation linked, retirement income provided by a generous Final Salary pension scheme, many prospective UK retirees are reliant on Defined Contribution (sometimes called Money Purchase) pension plans to provide for them when they stop working.

Unlike old-style Final Salary schemes, where all of the investment risk is borne by the former employer, Defined Contribution pensions are invested on an individual basis into global stock markets. Plan holders are then reliant on a combination of long term market returns and the wonders of compound growth to increase their retirement pot to a value that will allow them to achieve their desired level of expenditure in retirement.

Thanks to auto-enrolment rules introduced by the Government in 2012, many people’s retirement funds have accrued without them so much as opening an account. Clearly, some people have a far greater interest in managing their pension’s underlying investments than others, with the rise of online DIY platforms this has made it easier to do than ever, with many platforms offering unlimited trades and special offers on new fund launches.

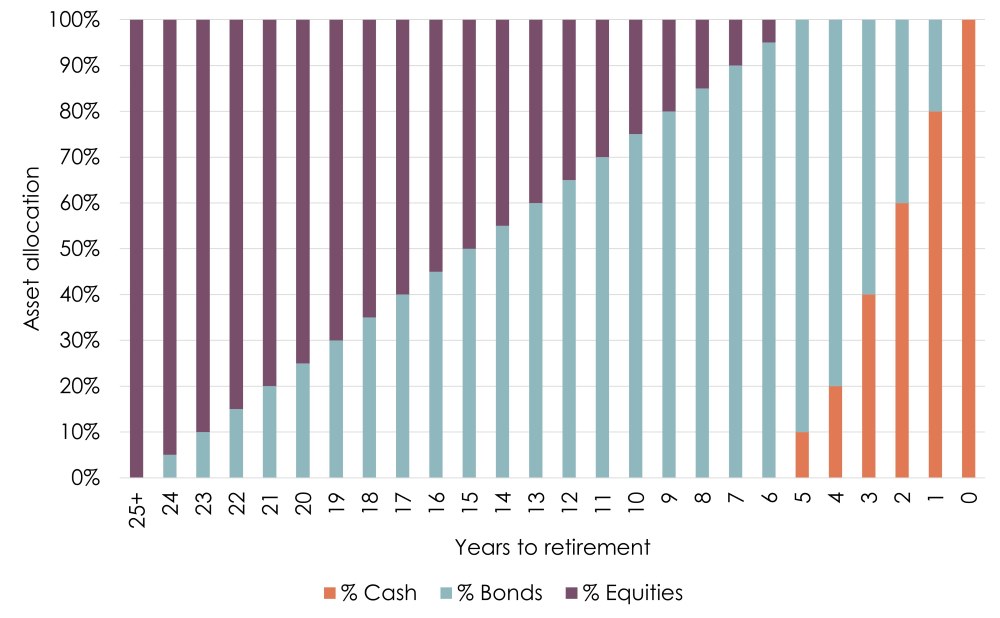

For those less interested in becoming the next Warren Buffett, your pension provider may have kindly sorted this all for you! The vast majority of workplace pension schemes are invested in a “lifestyling” strategy as default. This aims to put scheme members into riskier assets, like equities earlier in their careers to benefit from the greater levels of return that they have experienced historically. As a member moves closer to their nominated retirement age, the pension provider automatically reduces the level of riskier assets in the plan in favour of more conservative alternatives. The result is that the pension should be sat in one of the safest asset classes – usually government bonds or sometimes cash at their chosen retirement date, ready for the member to access their funds without being subject to the whims of market volatility.

How does lifestyling work?

Sounds great, right? How good of your pension provider, looking after that pot from that job in your twenties for all those years. If you’re beginning to get the sense that all of this sounds a little too good to be true, then that’s because it sort of is!

“Lifestyling” funds are fundamentally flawed for a number of reasons:

The first, is that the above strategy only works if the assets assumed to be risk free, actually are. The 2022 “Mini Budget” from Liz Truss and Kwasi Kwarteng brought it sharply into focus that bonds are not a risk-free asset. Some difficult conversations had to be had for individuals whose pensions had mostly lifestyled into bonds and cash and had thought because of this their pensions were secure. It even caused some to reconsider their retirement plans and put them off for a couple of years.

Another issue with lifestyling is that your workplace pension providers are understandably following the same glide path for everyone. Retirement planning is much more nuanced than this but workplace pension providers such as Royal London, Scottish Widows, Aviva, Aegon etc do not have the capacity to speak to each of their customers and understand what they actually need their pension pots to do for them over the long-term, from an income and lifestyle perspective.

The last issue we would like to highlight with lifestyling, is that the notion of having a pension entirely de-risked ready for the day you retire only makes sense if you are planning to use the whole pot to purchase an annuity. Due to rises in bond yields, annuity rates increased steadily from 2022 to the extent that they now present an option worth considering for certain retirees, for the first time in many years.

With this being said, annuities are by no means right for everyone. For many people, drawing upon their pension pot(s) flexibly, either through regular income payments or ad hoc withdrawals, will be the way in which they access their retirement funds.

The ONS estimates that someone at the average retirement age of 65 in the UK in 2025 can expect to live to on average a further 20 years for men on average, and 23 years for women.

This means two things; firstly that there is good chance that your pension will need to last you at least 20 years, but potentially much longer; and secondly, and related to the previous point - some of your pension may not be touched for another 20 years. Therefore, this element of your pot should not take the same level of risk and have the same investment strategy as the money you will be drawing upon in the first few years of retirement, which should be sat in cash ready for you to access.

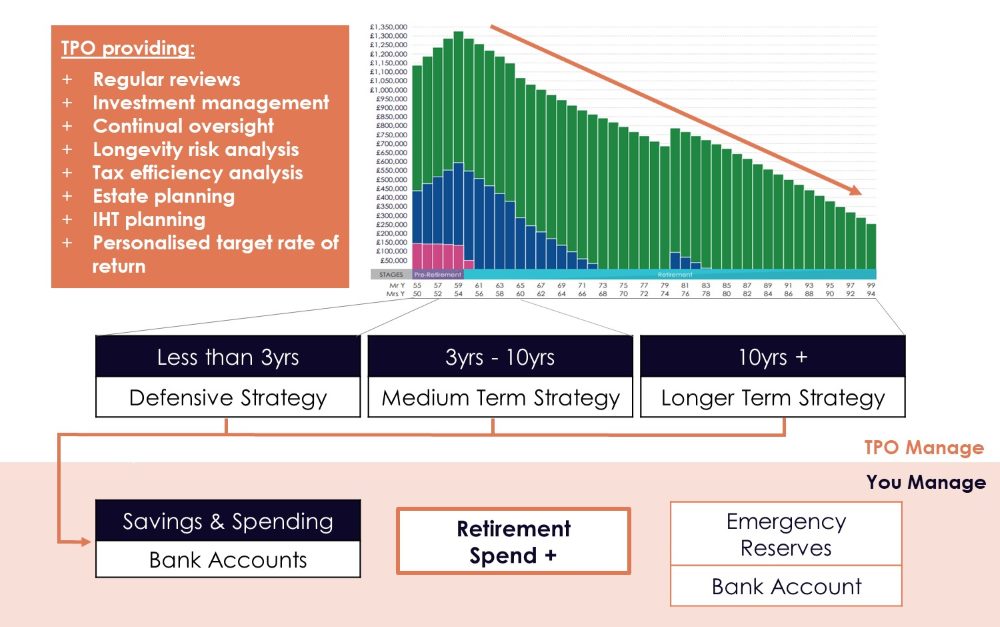

Segmenting your pension into different pots: the three pot plan

This is by no means anything ground-breaking; by segmenting your pension across different strategies, you are simply taking advantage of timescales. This means that your longest term money can work harder for you, but that the money you need to fund the next few years of living is sat in cash, taking no investment risk.

It may not always be the case that individuals hold significant levels of cash personally, in bank or building society savings or national savings and investment accounts. Nevertheless, holding cash for short-term income requirements can still be achieved. How? By holding a modern Self-Invested Personal Pension (SIPP) which can hold some of its investments in cash accounts or Money Market portfolios.

By holding a few years’ worth of expenditure in cash you give yourself time to ride out any of the shorter-term volatility in markets, meaning you are never forced to sell down upon your invested wealth at an inopportune time in market cycles in order to fund your day-to-day expenditure needs. Luckily, with interest rates still relatively high, the returns from holding cash are far better than anything we saw for many years.

As the above illustrates, planning appropriately is vital in ensuring sustainability throughout what will hopefully be a long and enjoyable retirement. Making sure that a robust retirement strategy is in place well in advance of actually retiring will allow your money to work as hard as possible for you, whilst also ensuring that you can continue to live your dream retirement without the need to worry about the ups and downs in markets.

Retirement Calculator

A useful tool to get a basic understanding of how much you may need is our retirement calculator. From your own inputs, you will be able to forecast an estimate of the pension income you will get when you retire and receive a target retirement income to aim for based on your choices.

How can we help?

The above is purely an example of a tool we always use with our clients, cash flow modelling. This is especially useful to both us and our clients at determining what they need their assets to do for them over the long-term and identify the different time horizons ahead of them before accessing certain proportions of their wealth.

If you’d like to learn more about how you can plan your own comfortable retirement, why not get in touch and speak to one of our advisers. We’re currently offering anyone with £100,000 in pensions, savings or investments a free initial consultation worth £500.

Arrange your free initial consultation

The information in this article is based on current laws and regulations which are subject to change as at future legislations.

A pension is a long term investment. The fund value may fluctuate and can go down. Your eventual income may depend on the size of the fund at retirement, future interest rates and tax legislation.

The Financial Conduct Authority (FCA) do not regulate estate or cash flow planning, or tax advice.