Skip to main content

Skip to main content

The Stealth Tax Squeeze

A new report has highlighted the growing impact of frozen tax allowances in the UK, with some thresholds remaining unchanged for more than four decades.

Research from Association of Taxation Technicians (ATT) found that numerous allowances have remained static for decades, resulting in taxpayers paying more in real terms without any formal increase in tax rates – a policy by the Government known more informally as ‘stealth tax’.

ATT argues that many tax reliefs are overdue a comprehensive review, as years of inflation have steadily reduced their real-world value through fiscal drag.

So, who’s being affected by ‘stealth taxes’?

Almost everyone will in some way or another be losing money to stealth taxes.

Inheritance tax provides some of the clearest examples. The nil-rate band, which determines how much of an estate can be passed on free from inheritance tax, currently remains at £325,000 per individual. This threshold was last increased 17 years ago and is now scheduled to stay frozen until 2031. According to the ATT report, if it had been adjusted in line with inflation, it would stand at approximately £525,000 today, around 60 per cent higher than its current level.

The same pattern can be seen across other inheritance tax exemptions. The annual gifting allowance has been fixed at £3,000 since 1981. Using the Bank of England’s inflation calculator, the ATT estimates that an inflation-linked equivalent would now be around £11,800, almost four times the existing allowance.

Meanwhile, the wedding gift exemption has remained unchanged at £5,000 since 1975, having originally been introduced under the capital transfer tax regime before inheritance tax existed in its current form. Had it increased in line with inflation over that period, it would now be worth £39,876, representing a rise of 697 per cent. With UK weddings in 2026 costing on average an eye watering £20,604, that missed 697 per cent will come with an especially nasty sting for newly weds.

The report also found that savers have been affected by the same phenomenon. Basic-rate taxpayers can currently receive up to £1,000 of savings interest tax-free under the personal savings allowance, while higher-rate taxpayers are entitled to £500. Had these limits risen alongside inflation since their introduction in 2016, they would now be worth roughly £1,400 and £700 respectively.

Homeowners benefiting from the Rent a Room scheme have also seen the value of their tax break eroded. The scheme's £7,500 tax-free income limit has not increased since 2016. If it had kept pace with inflation, it would now be closer to £10,500.

Not even those saving into their pensions have been able to escape the stealth tax net. Individuals without relevant earnings can contribute £2,880 each year to a pension, which becomes £3,600 after tax relief is added. This allowance has remained unchanged since 2000. If uprated for inflation, it would be approximately £5,500 net, or £6,850 including tax relief.

The forever frozen allowances

It has become the new norm for each Government to announce a further freeze on allowances, kicking the can down the road with each successive freeze, all the while taxpayers are being forced to hand over increasing amounts as fiscal drag pulls them ever further beyond the outdated thresholds.

One example of this is inheritance tax (IHT). Total IHT receipts collected by the Government has been steadily on the rise since the IHT threshold freeze.

This was initially announced by the then Chancellor, Rishi Sunak, in his 2021 Budget. The Budget outlined that the IHT threshold would be frozen for five years until 2026. However, after ex-Chancellor Jeremy Hunt’s 2023 Autumn Statement, it was confirmed that the freeze would be extended a further two years until April 2028, and then after Rachel Reeves’ 2024 Autumn Statement, this was extended once again a further two years until April 2030, and finally after her 2025 Autumn budget, it was again extended, this time until April 2031.

Many have been calling this a clear example of stealth taxes, as the freeze ultimately means an increasing number of Britons will fall into the tax threshold each year until the freeze ends in April 2031 – if it indeed does end and hasn’t been extended again by that time – and by then the Government will have collected billions of pounds worth of extra IHT from the taxpayer.

If you want to find out more, why not give us a call on 0333 323 9065 or book a free non-committal initial consultation with one of our chartered financial advisers to find out how can help.

Arrange a free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning, tax or estate planning.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

What should I do with my pension lump sum?

If you have already retired, or if you are approaching this milestone, you have probably been thinking about what you should do with your pension lump sum. Should you take it now so you can spend or gift it, should you leave it where it is to maximise the potential tax-free return or should you withdraw it in stages to provide a tax efficient income?

The answer will likely depend on your personal circumstances and your overall retirement objectives. Before you take anything, make sure you understand what type of pension you have, when you can access it, how tax works, and what taking money out now could mean for the rest of your retirement.

For most people with a defined contribution pension, you can access your lump sum from the age of 55 (rising to 57 from April 2028) and you can normally take up to 25% tax free, subject to the lump sum allowance of £268,275.

What is a defined contribution pension?

A defined contribution (DC) pension is a pension where you build up a pot of money over time through your and your employer's contributions, tax relief from the government, and investment growth. At the point of your retirement, you will not necessarily receive a guaranteed income, but instead, you will have an amount of money you can withdraw and spend flexibly to meet your life expenditure requirements. This means the responsibility is on you to make sure any withdrawals are sustainable so that this money will last for the rest of your life.

When it comes to how you might use your defined contribution pension, you might take some tax-free cash, leave the rest invested, draw income gradually, or use some or all of it to buy a guaranteed income in the form of an annuity. These decisions can be daunting as you are effectively making decisions that will impact you for the rest of your life, and this is where having a solid financial plan can support the decision-making process.

What type of pension do I have?

This is the first question to answer before doing anything with your lump sum because your options depend heavily on the pension type you have. And in some cases, you may have a mix of different types of pensions.

Broadly, most people will have either a defined contribution pension or a defined benefit (DB) pension, which is often called a final salary pension. A defined benefit pension typically pays a secure income for life based on your salary and length of service, rather than giving you a pension pot to manage yourself, providing a level of security not automatically achieved from a defined contribution pension. Defined benefit pensions can come with a decision whether to draw a tax-free lump sum in return for a reduced level of income. This can be an attractive option to pay for a nice retirement holiday, or to give to your children, but again, this decision should be made with the long-term in mind.

One way to understand the type of pension you hold, is to review the paperwork you have received from your provider. If your statement refers to a projected pot value, fund choices, or investment performance, it is likely a defined contribution pot. If it talks about an annual income payable at a normal retirement age based on service and salary, it is more likely defined benefit. Many people will have more than one pension, and it is not unusual to have a mix. That is why it is worth checking each scheme individually rather than assuming they will all provide a retirement income in the same way.

When can I take money from my pension?

For private pensions, the earliest age you can usually take money is 55 and this is set to rise to 57 from April 2028. In some cases, you may be able to access benefits earlier because of ill health, but for most savers, the normal minimum pension age applies. Importantly, reaching the age when you can access your pension does not mean you have to take it straight away. Some retirees may benefit from waiting if they do not yet need the money, because leaving the pension untouched can give investments more time to grow and delay the tax decisions that come with withdrawals.

This is where the real decision starts. If you need cash to clear expensive debt, support your lifestyle, or create a buffer in retirement, taking a lump sum could make sense. If you are still working, still contributing, and do not need the money yet, rushing to take it can be a costly decision. A pension is often one of the most tax efficient places to keep long-term retirement savings, so taking cash just because you can, is not always the best move.

Am I taxed on my pension?

Usually, yes, at least on part of it. Most people can take up to 25% of their defined contribution pension tax-free, subject to an overall tax free cash lump sum allowance of £268,275. The remaining 75% is usually taxable as income when drawn. That means the amount of tax you pay depends on how much you withdraw in that tax year and what other income you already have. For the 2026/27 tax year, the standard Personal Allowance is £12,570, basic rate tax is charged on the next £37,700, and the higher rate tax applies to the next £74,870 for England, Wales, and Northern Ireland.

This is why taking your whole pension in one go can result in a nasty surprise. Even if 25% is tax-free, the taxable balance may push you into a higher or additional rate band in that year (or potentially reduce or remove your personal allowance for income over £100,000). Providers also often use a temporary or emergency tax code on the first payment, which can result in too much tax being deducted upfront. In some cases, you can reclaim overpaid tax from HMRC rather than waiting until the end of the tax year.

How can I take money from my defined contribution pension?

You usually have a few main routes. One option is to take up to 25% tax free and leave the rest invested in a drawdown scheme, which essentially is an investment that you draw an income from, taking taxable income only when you need it. This can suit people who want flexibility and are comfortable with investment risk, but it does mean your money remains exposed to market ups and downs and there is no guarantee it will last for life.

Another option is to take up to 25% tax free and use the rest to buy an annuity, which gives you a guaranteed income for the rest of your life. This can be attractive if certainty matters more to you than flexibility. The trade-off is that once an annuity is set up, you cannot reverse the decision, and the rate you secure depends on market conditions and your circumstances at the time.

You can also take your pension as one or more lump sums. In practice, that can mean taking the whole pot in one payment or drawing cash out in stages. This can work well if you want control, but it needs care. Large withdrawals can create unnecessary tax burdens, and once money leaves the pension it loses some of the protection and tax advantages it had while inside the pension account wrapper.

Can I choose more than one way to take my money?

Yes, and for many people that is where the best answer lies. You do not always have to pick a single option and stick with it. You might take some tax-free cash for short term needs, leave part of the pot invested for later, and use another part to buy guaranteed income. If you have more than one pension pot, you can also use different options for different pensions. That can give you a better balance between flexibility, security, and tax efficiency.

What if I am still working?

So far, we have just focused on planning ahead for retirement, but what if you are still working and have a requirement or preference to draw from your pension? In this scenario, just drawing your tax-free cash allowance will not typically restrict the amount that you can contribute to a pension in the future, but taking taxable income flexibly often does. This activates the Money Purchase Annual Allowance, which reduces your annual pension contribution allowance from £60,000 to £10,000, which can matter a great deal if you are still working or may want to keep contributing.

Another important consideration is HMRC’s ‘Tax-Free Cash Recycling Rules’. These rules say you cannot take a tax-free lump sum from your pension with the intention of paying it back in to gain further tax relief. While this sounds straightforward, it can become more complex in practice and requires careful thought. A common example is where someone plans to draw a tax-free lump sum while they are still working, perhaps to repay their mortgage. Once the mortgage is cleared, they may find they have extra disposable income and decide to increase contributions to their workplace pension.

Although the withdrawal and the increased contributions may appear unrelated, they could still be viewed as linked under the rules. This means the arrangement could breach HMRC guidelines and potentially lead to a significant tax charge.

If you are considering a similar approach, it’s sensible to speak with a financial adviser to ensure you don’t face any unexpected tax consequences.

Speak to a pension specialist today

In most cases, before making any irreversible decisions it is best to pause and look at the bigger picture. Consider what income you will need, what secure income you already have, whether you are still working, how much tax you may pay, and whether taking cash now could reduce your options later. A pension lump sum can be useful, but it should support your retirement plan rather than drive it.

A good pension specialist can help you work through the options and considerations clearly, while helping to guide you through this decision-making process to ensure the action taken is in line with your requirements, not only now, but for the rest of your life. Most importantly, this can help you avoid turning a valuable pension into an avoidable tax bill or a short-term fix that weakens your long-term financial security.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The information is based upon our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

The value of investments can go down as well as up, you may not get back what you originally invested. The FCA does not regulate tax, estate or cash flow planning.

Inflation drops to 2.8%... but can it last?

The rate of inflation in the UK has dropped more than anticipated to 2.8% in the year to April, according to the latest figures from the Office for National Statistics (ONS). This is a notable drop from the 3.3% figure in the year to March.

Inflation continued to ease even as fuel costs climbed in the wake of the Iran conflict.

Data from the ONS showed petrol averaged 156.8p per litre last month, marking its highest level since November 2022. Diesel prices also jumped by more than 30p in April, pushing the average cost up to 190p per litre, the highest recorded since July 2022.

According to the RAC, petrol prices have continued to rise in May, reaching a new peak of 158.52p per litre on Tuesday.

So why has inflation fallen this time, and will it stick?

According to the ONS, energy costs had fallen thanks to a combination of reduced wholesale prices and the government’s energy bill support measures introduced before the Iran conflict began.

But economists are warning that inflation is likely to be on the rise again soon, potentially hitting around 4% by the end of the year, with ongoing tensions in the Middle East continuing to drive up global prices.

It’s also important to note that it can often take about a year for food supply cost changes to truly be reflected in food prices in the UK, so there are likely to be some price shocks as the economy catches up to the supply chain issues caused by the conflict.

What is inflation and how is it measured?

Inflation is a measure of how the prices of goods and services have increased over time. Goods are tangible items sold to customers, such as food, while services are tasks performed for the benefit of recipients, such as a haircut. Generally, this increase is measured by considering the cost of things today compared to how much they cost a year ago. The average increase between these prices is demonstrated in the inflation rate.

Rising inflation directly affects the cost of living. For example, if the price of a bottle of milk is £1, and inflation is increasing by 5%, then your bottle of milk will cost you 5p more. Or, in other words, the spending power of your money has decreased by 5%.

Ideally, the Government wants to keep inflation low and stable. The general mandated target for the Bank of England is 2%.

Anything significantly above or below this target is thought to cause issues for the economy.

The cost of living surged in recent years, with inflation peaking at 11% in 2022 - way above the Bank of England's 2% target, partly due to the increase in energy prices following Russia's invasion of Ukraine.

While the rate has dropped, falling inflation does not mean the goods and services are coming down in price overall, it is just that they are rising at a slower pace.

Our chartered financial advisers are expert and unbiased, meaning that they can give whole of market advice, and so are best placed to give you a plan tailored exactly to your personal financial goals.

If you’d like to know more, request a free non-committal initial consultation with one of our team or give us a call on 0333 323 9065 and get in touch.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

What is the threshold for higher rate tax?

Understanding when higher rate tax applies is an important part of making informed financial decisions. While tax can often feel complicated, the basic structure is more straightforward than many people expect. Knowing how much you can earn before moving into a higher band, what counts as taxable income and what allowances may be available, can help you plan more effectively and avoid surprises.

In the UK, Income Tax is charged at different rates depending on how much taxable income you receive. For many people, the key question is when earnings move beyond the basic rate and into the higher rate band. That threshold matters because it affects how much of your income you keep, how you approach pension contributions and how you think about wider financial planning.

Arrange your free initial consultation

Should I pay any Income Tax?

You only pay Income Tax on taxable income above the allowances available to you. For most people, that starts once income rises above the standard Personal Allowance of £12,570. If your earnings stay below that level, you will often have no Income Tax to pay, although there are exceptions depending on the type of income you receive and whether you qualify for any extra allowances.

It is also worth remembering that Income Tax is not charged on every type of money in the same way. Earnings from work, pension income, rental income and some savings income can all be taxed differently, and some people will have tax deducted through PAYE while others need to report income through Self-Assessment.

In practice, the question is not simply whether you earn money, but how much taxable income you have after any allowances and reliefs are taken into account.

When do you pay higher rate tax?

If you live in England, Wales or Northern Ireland, you start paying higher rate tax when your taxable income goes above £50,270. Income between £12,571 and £50,270 is taxed at the basic rate of 20 per cent, and income from £50,271 to £125,140 is taxed at 40 per cent. Above £125,140, the additional rate is 45 per cent. These are the current bands published by GOV.UK for the 2026 to 2027 tax year.

Scotland uses different Income Tax bands on earned income. There, the higher rate is 42 per cent and begins at £43,663 if you have the standard Personal Allowance, with an advanced rate of 45 per cent above £75,000 and a top rate of 48 per cent above £125,140. That means a Scottish taxpayer can move into higher rate tax sooner than someone elsewhere in the UK.

One detail that often catches people out is that crossing the higher rate threshold does not mean all of your income is taxed at 40 per cent. Only the part above the threshold is taxed at that rate. This is why a pay rise that takes you over the line is still usually beneficial, even if more of your income is taxed.

What is a Personal Allowance?

The Personal Allowance is the amount of income you can usually receive before paying Income Tax. For the 2026 to 2027 tax year, the standard figure is £12,570. For most employees and pensioners, this is the foundation of their tax calculation. It reduces the amount of income that is exposed to tax bands and helps determine when basic or higher rate tax starts to apply.

There is another important point here for higher earners. Once your adjusted net income goes above £100,000, your Personal Allowance is reduced by £1 for every £2 above that level. It falls to zero once income reaches £125,140. This creates a particularly harsh pinch point because you are not only paying higher rate tax, you are also losing part of your tax free allowance as income rises. This is where what’s known as the 60% tax trap kicks in, as it creates an effective 60% tax rate when taking income tax and reduced tax free allowances into consideration. Add in National Insurance and you’re paying a 62% effective rate.

What is Income Tax used for?

Income Tax is one of the main ways the government raises money to fund public services. HMRC states plainly that it collects the money that pays for the UK’s public services. GOV.UK also provides taxpayers with an annual summary showing how Income Tax and National Insurance contributions feed into government spending.

In broad terms, that revenue helps support areas such as health, education, welfare, transport, defence and day to day public administration. The Office for National Statistics also notes that taxes make up the majority of government income. So while Income Tax can feel like a deduction that disappears from your payslip, it remains one of the central pillars of how the state funds essential services.

How much Income Tax will I pay?

That depends on where you live in the UK and how much taxable income you have. In England, Wales and Northern Ireland, someone with taxable income of £60,000 and the standard Personal Allowance would pay no tax on the first £12,570, 20 per cent on the next £37,700 and 40 per cent on the remaining £9,730. That works out as £7,540 at basic rate and £3,892 at higher rate, for a total Income Tax bill of £11,432. The key point is that the higher rate only applies to the slice above £50,270. This calculation follows the current GOV.UK bands.

If you are in Scotland, the same salary can produce a different result because the bands are different. The tax system is not uniform across the UK, so using the right set of rates matters. This is especially relevant for people who are comparing job offers, approaching retirement, drawing income from multiple sources or trying to decide how much of a bonus to take as salary.

A further complication is that your tax bill can change if your Personal Allowance is reduced, if you receive taxable benefits, or if part of your income comes from dividends or savings. Income Tax is simple at the headline level, but once income sources multiply, the true figure can move quickly.

It is also worth understanding the order in which different types of income are taxed, as this can catch people out. Non savings income is taxed first. This includes earnings from employment, self employed profits, pension income and rental income. Savings income is taxed next, which includes things like interest from bank and building society accounts. Dividend income is taxed last. This matters because your non savings income uses up your Personal Allowance and tax bands before savings interest and dividends are taken into account, which can mean those later sources of income are taxed at a higher rate than expected.

For example, if someone in England has a salary of £45,000, savings interest of £3,000 and dividend income of £2,000, their salary is taxed first and uses up all of their Personal Allowance as well as most of the basic rate band. The savings interest then sits on top of that salary, and the dividend income sits on top of both. Even though none of the income sources looks especially large on its own, the order they are taxed in can push part of the interest or dividends into a higher band. That is why it is so important to look at your total income as a whole rather than viewing each source in isolation.

How to minimise the tax you pay

The starting point is to make full use of the allowances and reliefs that are already built into the system. Pension contributions can be particularly valuable because by paying your relief at source (so paying into a pension without the deduction of basic rate tax) this may increase your basic rate tax band which in turn can reduce the amount of income that will be taxed at the higher rate tax band. This can help you reduce the amount of tax you pay at the higher rate or preserve your Personal Allowance if income is above £100,000.

ISAs can also play an important role because returns within an ISA are sheltered from Income Tax and Capital Gains Tax. Salary sacrifice, where available, may improve tax efficiency too, depending on your circumstances. For couples, holding assets and drawing income in the most tax efficient name can also make a meaningful difference over time. None of this is about avoiding tax. It is about using the rules properly and planning ahead rather than reacting once the tax year has ended.

This is where financial planning becomes useful. The higher rate threshold is a point where decisions about pensions, remuneration, investment wrappers and income timing can start to have a much bigger impact. Knowing where the threshold sits is helpful. Structuring your finances around it is where the real value often lies.

If you want to find out more about minimising the amount of tax you might have to pay, you can request a free non-committal initial consultation with one of our team or give us a call on 0333 323 9065 and get in touch.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age).

The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

The information contained in this article is based on our understanding of legislation, whether proposed or in force, and market practice at the time of writing. Levels, bases and reliefs from taxation may be subject to change.

What is salary sacrifice for pensions?

Pensions remain one of the most tax-efficient ways to save for retirement, and there are several ways to build up your pot through the workplace. One option you may have heard of is salary sacrifice, which allows you to give up part of your salary in return for your employer paying more into your pension.

Under the current rules, this can be a highly efficient way to save, as it may reduce National Insurance costs for both you and your employer. But the rules are changing from April 2029, when the National Insurance benefit will be restricted. That means now could be a good time to understand how salary sacrifice works and consider whether you can make the most of it while the current advantages are still available.

Arrange your free initial consultation

What is salary sacrifice?

Salary sacrifice is an arrangement where you agree to give up part of your gross salary and, in return, your employer pays that amount into your pension instead. In practical terms, your contractual pay is reduced and your pension contribution is made by the employer rather than being taken from your pay afterwards. That matters because salary sacrifice changes how Income Tax and National Insurance are calculated on your earnings.

For many workplace pension members, it is one of the simplest ways to make pension saving more efficient. Instead of paying into a pension from taxed pay, the contribution is made before your salary reaches your bank account. This can improve take home pay, increase the amount going into your pension, or do a bit of both, depending on how your employer has set the scheme up.

How does salary sacrifice help with pensions?

The main attraction of salary sacrifice is that it can make pension saving more efficient without requiring you to invest more of your disposable income. Because your salary is reduced, you do not pay Income Tax or National insurance on the amount being sacrificed, therefore, overall you pay less National Insurance and Income Tax because you have less salary. Your employer also pays less employer National Insurance on that part of pay.

Some employers keep their own National Insurance saving, while others choose to add some or all of it to your pension. When that happens, salary sacrifice can become especially powerful because the pension receives more money than it would under a standard employee contribution arrangement.

There can also be wider planning benefits. Salary sacrifice lowers taxable pay and adjusted net income, which may help some people tipping into higher tax thresholds linked to the personal allowance taper or support eligibility for certain forms of childcare support. That will remain the case even after the future salary sacrifice reform takes effect.

What are the tax savings with salary sacrifice?

Employee savings

For employees, the saving comes through lower National Insurance and lower Income Tax as no National Insurance or Income Tax is payable on the amount sacrificed. Under the current rules, salary sacrifice pension contributions reduce the pay on which those deductions are worked out. Both Income Tax and National Insurance are calculated after the sacrifice has been made.

That means a pension saver can often build a larger retirement pot more efficiently than through an ordinary deduction from net pay. For basic rate taxpayers the result is often straightforward and visible on the payslip. For higher earners, the benefit can be even more noticeable, especially if salary sacrifice is used for regular contributions or bonus sacrifice. The exact gain depends on income level, National Insurance band and whether the employer shares any of its own saving.

Employer savings

Employers also benefit because pension contributions are not normally subject to employer National Insurance, while salary is. The standard employer National Insurance rate is 15 per cent on earnings above the relevant threshold for 2026 to 2027, which is why salary sacrifice can reduce payroll costs.

That saving creates choices. Some firms use it to offset rising employment costs. Others pass some or all of it into employees’ pensions, which can make salary sacrifice particularly attractive as part of a workplace benefits package. For businesses trying to improve pension engagement without sharply increasing overall reward spend, salary sacrifice has often looked like a practical middle ground.

Are there any disadvantages to salary sacrifice?

Salary sacrifice is not right for everyone. Because it reduces contractual salary, it can affect anything linked to your official pay figure. In some cases that may include mortgage affordability assessments, redundancy calculations, life cover linked to salary, or statutory payments such as maternity pay, paternity pay or sick pay. HMRC says salary sacrifice can reduce statutory pay and, in some circumstances, can remove entitlement if earnings fall below the lower earnings limit.

There is also a practical limit for lower earners. A salary sacrifice arrangement cannot reduce cash pay below the National Minimum Wage or National Living Wage. That means some employees, especially those on lower or variable earnings, may not be able to use it fully or at all.

This is why salary sacrifice should be seen as a planning tool rather than a default choice. The savings can be valuable, but the wider impact on pay related benefits and borrowing needs to be checked first.

Who benefits from salary sacrifice?

In broad terms, salary sacrifice tends to work best for employees with enough headroom above minimum wage, stable earnings and a workplace pension scheme that is already well organised. It can be particularly useful for higher earners, people making larger pension contributions and employees whose employer shares its own National Insurance saving.

Employers can benefit too, especially if they want a tax efficient way to support pension saving while managing payroll costs. HMRC commissioned research published in 2025 showing that salary sacrifice was already a significant feature of employer pension thinking, and that potential National Insurance reform could influence whether employers continue to offer it in the same way.

That said, the biggest winners have often been those making sizeable pension contributions through salary sacrifice year after year. That point matters because it helps explain why the government has now decided to intervene.

What is changing?

The government announced at Autumn Budget 2025 that the National Insurance advantage of pension salary sacrifice will be restricted from 6 April 2029. From that date, only the first £2,000 a year of employee pension contributions made through salary sacrifice will remain exempt from National Insurance. Any amount above that will be subject to both employee and employer National Insurance. Pension contributions made this way will still remain exempt from Income Tax, subject to the usual pension limits.

This is a significant shift. At the moment, there is no equivalent National Insurance cap on pension contributions made through salary sacrifice. From April 2029, the structure remains in place, but much of the National Insurance advantage disappears once contributions go over the new annual limit.

How much could pension savers using salary sacrifice lose?

The answer depends on how much is being sacrificed above the new £2,000 limit and which National Insurance rate applies to the employee.

For modest contributors, the impact may be limited. For larger pension savers, especially those using salary sacrifice heavily, the difference could be meaningful. The Office for Budget Responsibility estimate cited by the House of Commons suggests the reform will raise £4.7 billion in 2029 to 2030 and £2.6 billion in 2030 to 2031, which underlines how much value the current National Insurance relief provides.

The people most likely to feel the change are those sacrificing well above £2,000 a year, including higher earners and employees using salary sacrifice for bonus planning. They may still want to use salary sacrifice, because the Income Tax treatment remains valuable, but the numbers will look less compelling than they do today.

Why has the government announced this change?

The government’s published explanation is that these reforms are aimed at tax reliefs whose cost has been rising and which disproportionately benefit wealthier individuals. In other words, ministers see the current rules as generous, expensive and unevenly distributed.

There is also a clear fiscal motive. The reform raises revenue without removing pension tax relief entirely. Salary sacrifice for pensions will continue, and contributions will still be exempt from Income Tax, but the National Insurance advantage will be narrower and more controlled. That allows the government to keep encouraging pension saving while collecting more from larger contributions.

Talk through your pension options

Salary sacrifice can still be a useful way to pay into a pension, but it is worth reviewing how well it fits your wider plans. It may still work well now, especially if your employer adds some of its own National Insurance saving into your pension, but the position could look less attractive once the rules change in April 2029.

One option is to keep using salary sacrifice if it remains efficient for your level of earnings and contribution. Another is to review how much you are sacrificing, especially if you pay in larger amounts and may be affected by the new £2,000 annual National Insurance exemption limit from 6 April 2029. It can also be sensible to check how a lower contractual salary could affect things like borrowing, statutory pay and other benefits.

The key is to prepare early. Salary sacrifice is still valuable, but those making larger pension contributions may want to review their approach before the new rules begin.

Arrange your free initial consultation

This article is for information only and does not constitute individual advice. The information provided in this article is based on the current allowances and legislation and is subject to change.

The Financial Conduct Authority (FCA) does not regulate trust or tax advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Your pension income could also be affected by the interest rates at the time you take your benefits. The tax implications of pension withdrawals will be based on your individual circumstances, tax legislation and regulation which are subject to change. You should seek advice to understand your options at retirement.

How much tax do you pay on your savings?

In the UK, the interest you earn on savings can count as taxable income once it reaches a certain threshold.

The amount you can earn before you reach this threshold is known as the ‘Personal Savings Allowance’. This is the amount of savings interest you can earn before tax is applied, depending on your Income Tax band.

It is different from your HMRC ‘Personal Allowance’, which is the amount of income you can earn each tax year before paying Income Tax. The two are often confused, but they do different jobs. Your Personal Allowance covers income more broadly, while your Personal Savings Allowance is specifically about interest earned on cash savings.

Arrange your free initial consultation

The basics about savings and tax

Contrary to what many people assume, savings are not always tax free. In the UK, the interest you earn on your savings can be taxable, depending on how much you receive and your Income Tax band. Many savers will not pay any tax, but it is still important to understand the limits.

The good news is that the rules are a bit more generous than many people realise. Before savings interest is taxed, several allowances may come into play. Your Personal Allowance can help, there is a starting rate for savings in some cases, and most savers also have a Personal Savings Allowance. Together, these can mean you earn some interest without paying any tax. And everyone can also take advantage of the Individual Savings Account (ISA) where any returns are free of any tax.

What types of savings interest are taxed?

The main type of savings income people think about is interest from bank and building society accounts, and that certainly can be taxed. But savings income is wider than that. It can also include interest from some credit union accounts and certain other savings products that pay interest outside a tax sheltered wrapper. In practice, if a product pays you interest and it is not a tax efficient account such as an ISA, there is a good chance it needs to be considered.

By contrast, interest earned inside an ISA does not count as taxable savings income. That is one of the reasons ISAs remain so useful, especially for higher earners or for people with larger cash balances who may go over their allowance elsewhere.

The tax treatment of children’s savings can also be different in some cases, especially where money has been given by a parent, so that is another area where it pays to be careful.

What is a Personal Savings Allowance?

The Personal Savings Allowance is the amount of savings interest you can receive each tax year before tax becomes due. It is linked to your Income Tax band rather than being the same for everyone. Basic rate taxpayers can earn up to £1,000 in savings interest tax free. Higher rate taxpayers have an allowance of £500. Additional rate taxpayers do not get any Personal Savings Allowance.

This allowance has become especially important in recent years because higher savings rates have pushed more people above it. Someone with a modest savings balance in cash may never notice the rules. Someone with a larger emergency fund or house deposit can cross the line much more quickly once interest rates start to rise. That does not mean saving is a mistake, but it does mean the tax position is worth checking.

How your personal savings allowance works

Your allowance is based on your highest rate of Income Tax. To work that out, HMRC looks at your other income and your savings interest together. That means your tax band is not judged in isolation from your savings. If your earnings already put you in the higher rate band, your Personal Savings Allowance is £500. If your income places you in the additional rate band, it will be nil.

There is also a starting rate for savings, which can help people on lower incomes. If your non savings income is low enough, you may be able to earn up to £5,000 in savings interest at a 0% starting rate. This is separate from the Personal Savings Allowance and can sit alongside it. In the right circumstances, that means someone with a lower income may be able to receive more interest before any tax is due.

What your Personal Savings Allowance includes

Your Personal Savings Allowance applies to savings income such as bank and building society interest. In simple terms, it covers the interest you receive from taxable savings accounts. HMRC says you should add the interest you have received to your other income when working out your tax position, which shows that the allowance is about savings income.

What does not need to be included is interest from tax free wrappers such as ISAs, because that interest is already outside of the tax net. It also does not mean all investment returns are treated the same way. Dividends, for example, have their own separate rules, and gains on investments follow different tax rules again. That is why it is important not to lump all savings and investments together as though they are taxed in the same way.

Exceeding your Personal Savings Allowance

If your savings interest goes above your Personal Savings Allowance, the excess is taxed at your usual rate for savings income. So a basic rate taxpayer would generally pay 20% on the amount above the allowance. A higher rate taxpayer would generally pay 40% on the excess. Additional rate taxpayers will also face a tax charge on all of their taxable savings interest at 45% because they do not receive the allowance.

It should also be noted that the tax rates on cash savings is increasing by 2% from 6th April 2027. So, a basic rate taxpayer will pay 22%, a higher rate taxpayer will pay 42% and an additional rate taxpayer will pay 47% on any taxable interest.

The Personal Savings Allowance can be used up more easily than people expect. As mentioned earlier, a large cash balance held for security can produce a sizeable amount of interest when rates are decent.

As an example. If your savings account is paying you 4.0%, you only need a balance of £25,000 to use up the whole of your basic rate allowance of £1,000 in a year. Everything above that £1,000 will be taxed.

In some cases, savers who have never had to think about tax on their interest before may suddenly need to. That is often the point where a review of account structure, ISA use, and wider financial planning becomes worthwhile.

Paying tax on savings interest

Banks and building societies pay interest gross, which means without deducting tax first. If tax is due, HMRC will usually collect it later. For many employees and pensioners, that is done by changing the tax code so the right amount is collected through PAYE. If you complete a Self Assessment tax return, savings interest is usually dealt with there instead.

That system can feel easy when it works properly, but it still leaves room for mistakes. If HMRC does not have the right information, or if your circumstances change during the year, the amount collected may not be exactly right. That is one reason it is sensible to keep an eye on how much interest your accounts are generating rather than assuming everything has been sorted automatically.

It is worth noting that most banks and building societies tell HMRC how much interest they have paid to their customers, so trying to ‘hide’ from HMRC is not advisable.

How to pay tax on savings and investments

As mentioned above, if you already file a Self Assessment return, you normally declare your taxable savings interest there. If you do not complete Self Assessment, HMRC may adjust your tax code to collect what is owed. Where tax has been deducted and should not have been, you may be able to reclaim it, including through form R40 in the appropriate cases.

The key point is that savings and investments should not be looked at in isolation. Cash interest, ISA allowances, dividend income, and other taxable returns all interact with your wider financial picture. A decision that looks sensible on one account can become less efficient when you step back and look at your full position. Good planning is often less about chasing the highest headline rate and more about keeping more of what you earn after tax.

Speak to an expert to protect your savings

Tax on savings is not always complicated, but it is easy to misunderstand. A lot depends on your income, your tax band, and where your money is held. What seems like a small detail can make a real difference once balances grow or interest rates improve. And don’t forget, using any unused allowance your spouse has can help minimise your tax bill when working as a couple.

Speaking to an expert can help you understand whether you are likely to pay tax, whether your cash is in the right place, and whether you could make better use of wrappers such as ISAs. The aim is not to make saving feel difficult. It is to help you keep your plans efficient, avoid unpleasant surprises, and make sure more of your money keeps working for you.

Arrange your free initial consultation

The Financial Conduct Authority (FCA) does not regulate cash flow planning or tax.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

ISA changes: why 2026/2027 tax year matters more

The start of the new tax year is often a good time to take stock of your finances, to review what you already have and consider what you need to do next. And in today’s environment, where every penny counts, making full use of the tax allowances that are still available has never been more important.

The ever-popular Individual Savings Account, or ISA is a good place to start. Like a lot of our tax allowances, the ISA allowance has been frozen for many years, so for the 2026/27 tax year, the overall ISA allowance remains at £20,000, offering one of the simplest and most effective ways to protect your savings and investments from tax on interest, dividends, and capital gains.

However, there are changes coming for those who favour the cash element of an Individual Savings Account (ISA).

Cash ISA allowance to be cut

Cash ISAs regained their popularity over the last few years, as interest rates increased, which led to savers paying more tax than they had for over a decade when interest rates were at rock bottom. There is now some £458 billion stashed away in cash ISAs, almost a quarter of the total amount held in cash savings. But for savers under the age of 65, the current tax year is the last chance to make use of the full ISA allowance for cash only deposits.

From 6 April 2027, the rules are set to change. Whilst the overall ISA allowance will remain at £20,000, only £12,000 of that can be deposited into a cash ISA for those aged under 65. To use the full allowance, the remaining £8,000 will need to be invested in a stocks and shares ISA.

To add insult to injury, at the same time that the cash ISA allowance is to be cut, the tax on savings interest will be increasing by 2%. So, a basic rate taxpayer will pay 22% on any taxable interest, it’s 42% for higher rate taxpayers and 47% for additional rate taxpayers, making the cash ISA even more valuable.

The good news is that those aged 65 and over are not affected by this change. They will still be able to place the full £20,000 into cash if they wish, a welcome exemption for older savers. But it highlights a broader policy direction, encouraging younger savers towards investment.

A nudge towards investing

Whilst the comfort of a cash ISA is understandable, particularly in volatile times, it’s important to be aware that inflation can quietly erode the value of savings, and even with improved interest rates, cash may struggle to deliver meaningful real returns over time if inflation is higher than the interest you are earning. So, it might be worth asking yourself whether a purely cash-based approach is the right strategy for the longer term.

This is where stocks and shares ISAs come into play. They are not without risk though as values can go down as well as up. But they offer the potential for growth that cash generally cannot match over the long term, as long as you are prepared to accept the inevitable bumps in the road. You can of course, choose investments that better reflect your own personal attitude to risk, which will help minimise any potential downs and ups.

These changes could therefore be viewed as a prompt to diversify if you don’t need access to your money for the longer term, so more than five years. Using some of your ISA allowance for investment could make a meaningful difference to your future financial health.

Use it or lose it

Given the upcoming changes, this tax year (2026/27) is an opportunity not to be wasted. If you are under 65 and prefer cash, it may make sense to maximise your cash ISA contributions while you still can.

And due to the ongoing conflict in the Middle East, with the expectation that inflation and therefore the Bank of England base rate could rise, savings rates have been increasing recently. Good news for savers, especially those who don’t also have debts.

So, if you have funds sitting in taxable accounts, now is the time to consider sheltering them, as once the tax year ends, you can’t carry it forward.

Don’t overlook the Lifetime ISA

Alongside the standard ISA options, there is also the valuable Lifetime ISA (LISA), which is available to those aged between 18 and 39. The LISA allows you to contribute up to £4,000 per tax year, which counts towards your overall £20,000 ISA allowance and the real attraction is the generous 25% government bonus. In simple terms, a £4,000 contribution is topped up to £5,000, an immediate and very attractive return, even before any interest of investment growth is added.

Traditionally, the LISA has served a dual purpose: helping people save for their first home or for retirement. However, it is currently under review, and there is growing speculation that the retirement element could be removed going forward, making it simply a product for first-time buyers.

In the meantime, for those eligible, it remains a compelling option, particularly if you are saving for your first home.

ISAs for the next generation

It’s also worth remembering that children have their own ISA allowance through the Junior ISA (JISA).

With a current annual allowance of £9,000 per year, the Junior ISA allows parents, grandparents, and others to build a tax-free savings pot on behalf of a child. It can be held in cash or invested, depending on your preference and time horizon.

There is, however, an important point to bear in mind: there is no access to the money until the child turns 18, at which point they gain full control of the account, which could have grown to a really significant amount. The funds become theirs to use as they wish, whether that’s for university, a car, a house deposit, or, indeed, something less sensible.

Alternatively, the funds can be rolled over into an adult ISA, retaining the tax-free status and allowing the savings habit to continue into adulthood.

For those who save for their children, it makes sense to have open conversations with them as they grow older, so that hopefully they will do the right thing with this valuable gift. Financial education is just as important as the savings themselves.

Time to take action

The beginning of the tax year is a great time to make use of your ISA allowance, for a couple of reasons.

First, during the ‘ISA season’ of which April is the pinnacle, cash savings providers tend to compete with each other, which pushes rates higher, providing plenty of choice.

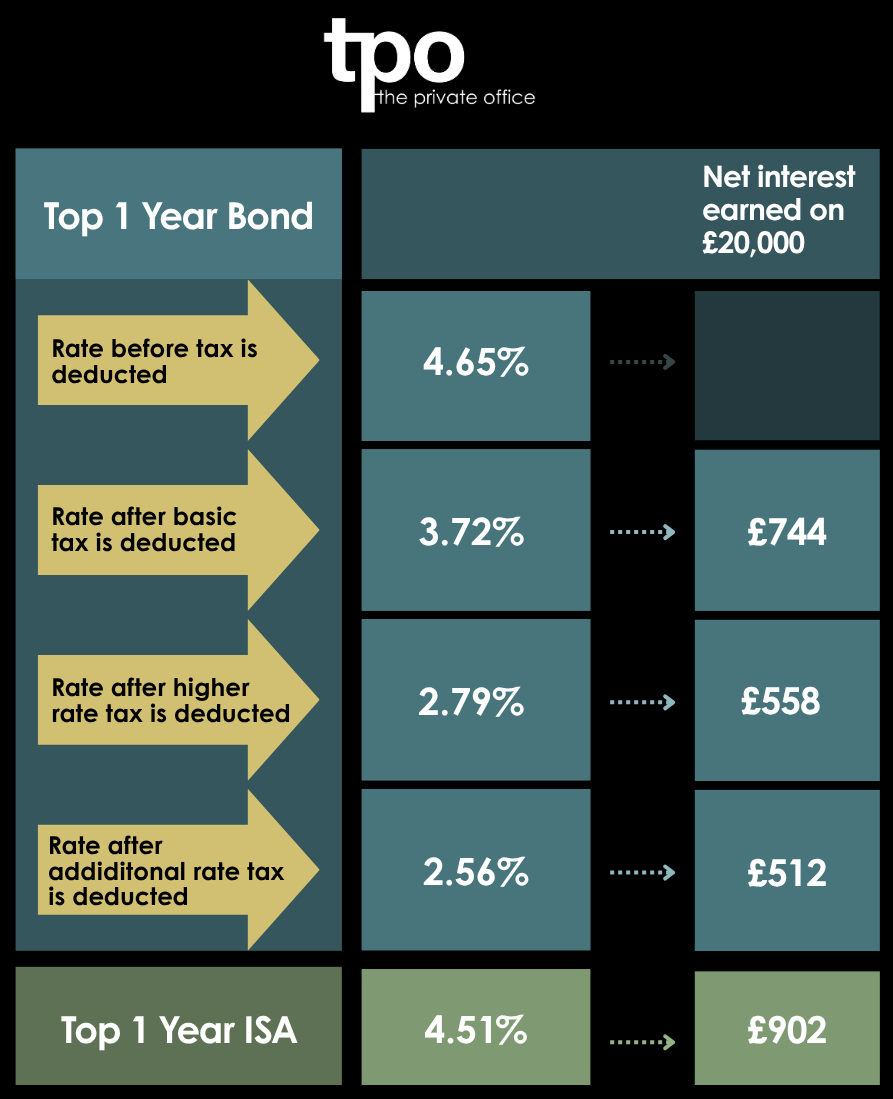

Secondly, why leave your cash in a taxable account any longer than you need to. Although often the headline rates on taxable fixed rate bonds may look higher than the same term cash ISAs, once you deduct income tax, you can earn far more in the tax-free ISA, as the table below illustrates:

Now is also a good time to review your old ISAs, to see if you could be earning more by switching. The key rule is vital though - never withdraw the funds yourself. Instead, always use the official ISA transfer process provided by your new provider, who will liaise directly with your existing bank or building society. If you take the money out and attempt to redeposit it, it could lose its ISA “wrapper” which crucially means you would forfeit the tax-free status tied to those historic allowances. Given that ISA allowances cannot be reinstated once lost, this is an irreversible and often costly mistake.

Reviewing your old ISAs whilst making the most of your new ISA allowance means that you can make your cash work as hard as possible, particularly important if we are to see inflation spiking upwards once again.

If you want to make your cash work harder, it is important to compare rates regularly and move money when better deals arise. In a market that is shifting and where relatively small rate differences can add up to hundreds of pounds over a year, staying informed is the best way to keep your savings working as hard as possible. Check our best buy tables for the most up to date savings rates.

Arrange your free initial consultation

Rates correct as at 07/04/2026.

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning.

Easter present for pensioners with inflation busting increase

Inflation held steady at 3% in the 12 months to February, matching expectations and unchanged from January, though it continues to sit above the Bank of England’s 2% target.

It should be noted this figure was recorded prior to the outbreak of conflict in the Middle East, which has since driven up the cost of energy and fuel, meaning inflation is expected to rise in the coming months.

Despite the sticky 3% rate of inflation, pensioners are set to receive higher state pension payments from Monday 6 April, during the first full week of the new tax year.

The main state pension rate is set to rise by 4.8% under the ‘triple lock’ system.

This established government policy ensures the state pension increases each year by the highest of inflation, average earnings growth, or 2.5%.

For this year’s adjustment, earnings growth was the deciding factor during the key reference period used to set the increase.

This means that pensioners are actually beating the rate of inflation for the start of the new tax year. And because the average earnings growth has now fallen below 4% according to ONS figures from November 2025 to January 2026, pensioners are also set to see a bigger increase than the workforce, since wages growth for the triple lock is calculated between May and July the previous year.

What is inflation and how is it measured?

Inflation is a measure of how the prices of goods and services have increased over time. Goods are tangible items sold to customers, such as food, while services are tasks performed for the benefit of recipients, such as a haircut. Generally, this increase is measured by considering the cost of things today compared to how much they cost a year ago. The average increase between these prices is demonstrated in the inflation rate.

Rising interest rates directly affects the cost of living. For example, if the price of a bottle of milk is £1, and inflation is increasing by 5%, then your bottle of milk will cost you 5p more. Or, in other words, the spending power of your money has decreased by 5%.

Ideally, the Government wants to keep inflation low and stable. The general mandated target for the Bank of England is 2%. Anything significantly above or below this target is thought to cause issues for the economy.

The cost of living surged in recent years, with inflation peaking at 11% in 2022 - way above the Bank of England's 2% target, partly due to the increase in energy prices following Russia's invasion of Ukraine.

While the rate has dropped significantly since then, falling inflation does not mean the goods and services are coming down in price overall, it is just that they are rising at a slower pace.

Our chartered advisers are unbiased, meaning that they can give whole of market advice, and so are best placed to give you a plan tailored exactly to your personal financial goals.

If you’d like to know more, request a free non-committal initial consultation with one of our team or give us a call on 0333 323 9065 and get in touch.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

Don’t panic about your financial future, just plan

At the time of writing the Middle East conflict is in full flow. The Straits of Hormuz are effectively closed, and markets are swinging on a daily basis depending upon whether Donald Trump has got out of the left hand side or right hand side of his bed. In short, no one has got the faintest idea what’s happening and by the time this article goes to print, for all I know, the war will be over, and markets would have jumped 10% or, things will have escalated and markets will have fallen 10%.

Arrange your free initial consultation

“Don’t panic Mr Mainwaring” blurted Corporal Jones, in virtually every episode of the classic BBC comedy, Dad’s Army. Of course, no one was panicking, except for Corporal Jones himself and in this state of blind panic, he was the least likely member of the platoon to be able to resolve the predicament they happened to be in. Panicking, generally, does not lead to sound decision making and certainly not sound financial decisions.

There are plenty of reasons to ‘panic’ in today’s world (financially and otherwise) but as Corporal Jones has shown us, panicking gets you nowhere. Life goes on, and the markets go on too and the worst thing investors can do is convince themselves that “this time it’s different”, that the end is nigh and that we all need to grow carrots and store drinking water in industrial quantities.

In their 2009 book “This Time is Different”, the economists Carmen Reinhart and Kenneth Rogoff argue that investors always fall for the trap of believing that the game is up and that capitalism is over and investing is no longer viable. There are always people who come out of the woodwork at these moments in time to endorse and bolster the naysayers, not because their views are valid but because the media is prepared to give them airtime. Funnily enough, we do not hear about them much when markets are doing well which, believe it or not, is most of the time.

The peace of mind a financial plan provides

I’m not pretending that the Iran war isn’t a threat to the world economies, far from it, but I wouldn’t like to bet on markets being lower in a year’s time to where they are now. They might be, of course, but if you want to safeguard yourself against inflation, history has taught us that market exposure is the best way to do it. Cash and bonds generally lose in real terms over the long term.

Markets tend to recover from shocks, whatever they are, and economists call this antifragility, which is the general principle that markets are able to adapt to new conditions. As one source of enterprise closes down, another one opens up and markets always sniff them out, if not immediately, then in time.

It is all well and good to say "don’t panic," but that is much easier to achieve if you actually have a plan in place. The major benefit of having a plan that you regularly revisit is the emotional peace of mind it provides. It moves you away from making knee-jerk reactions based on the morning's headlines and back towards a structured approach. If your personal circumstances change, or the government decides to shift the goalposts on taxes, a quick review of the plan will tell you exactly what needs to be adjusted. By keeping a close eye on your financial roadmap, you can ignore the noise of the markets, knowing that while the path might get a bit bumpy, you are still heading in the right direction.

What we already know

In addition to the “unknowns” (such as the Iran war), we also have the “known” events of future tax changes which are much favoured by the current Labour Government. On going stealth taxes, announced in 2021 as a short-term measure post Covid but now expected to continue until at least 2031. Dividend Tax increase and VCT relief reduction (April 2026); IHT on pensions (April 2027); Mansion Tax (2028) and Salary Sacrifice capping (2029).

In previous articles I have highlighted the dangers of not investing. Just to remind you, in the 20 years from 1st January 2004, $10,000 invested in the S&P 500 would have grown to $66,637 (an annualised growth rate of 9.7%). Had you missed the best 10 days during that 10 years the final sum would have been $29,154 (5.5% annualised growth rate). Take away the best 20 days and it’s $17,494 (2.8%). The message is, of course, stay invested and don’t try to call the markets.

As always, the key is to ensure that you have sufficient liquidity to ride out market volatility. For clients who are nearing retirement, they enter into the ‘decumulation’ - or ‘drawing down’ - phase of their investing life. That is, the scary moment when assets accumulated over decades must now step up to the plate and start delivering actual money to ensure a comfortable retirement. If you don’t plan this properly, you become exposed to what is known as “sequence risk”. This represents a significant threat to portfolios if investments are encashed to meet ongoing expenditure during a market downturn. Risk management planning is vital in retirement to ensure you avoid this pitfall. Investment portfolios need to remain invested, to protect them from long term real value erosion, but for decumulators, the higher risk elements must still be viewed as long term and kept invested for many years, if need be, to await a recovery if the downturn is severe. That’s why the cash buffer is important!

In January 2026, markets were looking bullish, economies were generally on the up and most market commentators were positive about the prospects of equity markets continuing to do well. So, what do we do? Keep calm and carry on investing, or, to quote another Dad’s Army character, hold our heads in our hands and say “we’re doomed!”.

But whatever you decide, the best approach is to have your own personal plan in place, review it with your professional advisers and above all, don’t panic!

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions.

The Financial Conduct Authority (FCA) does not regulate cash flow planning, estate planning, will writing, tax or trust advice.

A pension is a long-term investment not normally accessible until age 55 (57 from April 2028 unless the plan has a protected pension age). The value of your investments (and any income from them) can go down as well as up which would have an impact on the level of pension benefits available.

Past performance is not a reliable indicator of future performance.

Growth downgraded in Spring Forecast 2026

Rachel Reeves delivered her Spring Forecast this afternoon, which had been overshadowed before it even started by events in the Middle East.

As expected, the Spring Forecast (rather than Spring Statement as it has been referred to in previous years) did not include any fiscal changes, with Reeves previously committing to only holding one fiscal event each year, in the Autumn Budget.

By way of updates, Reeves announced that the Office for Budget Responsibility (OBR) had ‘adjusted the profile of GDP’ resulting in it downgrading its UK Growth projection for 2026 from 1.4% (as forecast in November 2025) to 1.1%, but the OBR increased its forecasts for 2027 (1.5% to 1.6%) and 2028 (again 1.5% to 1.6%). Reeves also heralded the interest rate cuts seen in recent months, but events in the Middle East have significantly reduced the chance of a further cut in March, given the inflationary oil and gas price rises seen since the weekend.

Therefore, the most important upcoming tax changes are those we already knew about, specifically:

- A 2% increase in dividend tax taking effect on 6 April 2026.

- VCT tax relief being cut from 30% to 20% on 6 April 2026.

- Business and Agricultural Relief limited to £2.5m per individual, with effect from 6 April 2026 – this importantly increased from the previously proposed £1m and can be passed between spouses if not used on first death.

- A 2% increase in savings and property taxes taking effect on 6 April 2027.

- A cap in Cash ISA contributions of £12,000 for under 65s with effect from 6 April 2027.

- Pensions forming part of estates for inheritance tax purposes from 6 April 2027.

- A Mansion Tax being introduced in April 2028.

- Salary Sacrifice pension contributions benefiting from National Insurance Contribution savings limited to £2,000 with effect from 6 April 2029.

- Income Tax thresholds frozen until April 2031.

If you would like to discuss the impact of the above on your personal financial situation, why not get in touch for a free initial conversation to see how we can help.

Arrange your free initial consultation

This article is intended for general information only, it does not constitute individual advice and should not be used to inform financial decisions

The Financial Conduct Authority (FCA) does not regulate estate planning or tax advice.