Skip to main content

Skip to main content

Election Season – Is a shift to the left, right for markets?

In last month’s update we touched upon the French and British general elections, however at the time of writing the UK election hadn’t yet taken place and the French election had only passed its first round. Now that both elections have concluded we can take a deeper dive into market reactions.

Arrange your free initial consultation

The election results

Before we get going it’s worth summarising recent events, starting with the UK. Pollsters had been predicting a Labour landslide, and while they overestimated the realised vote share for Labour, due to our first-past-the-post voting system this still translated into one of the largest majorities our parliament has seen. This result should provide the foundation for a stable government with the ability to enact its desired agenda.

In France results were less conclusive, in part due to their more proportional voting system. Le Pen’s National Rally party won the largest vote share of any individual party, however due to the fractured nature of their parliament, with three roughly equal coalitions, it seems unlikely that a government will be formed in the very near term. This will not provide the foundation for a stable government with the ability to smoothly enact its desired agenda.

Market reactions to the UK election result

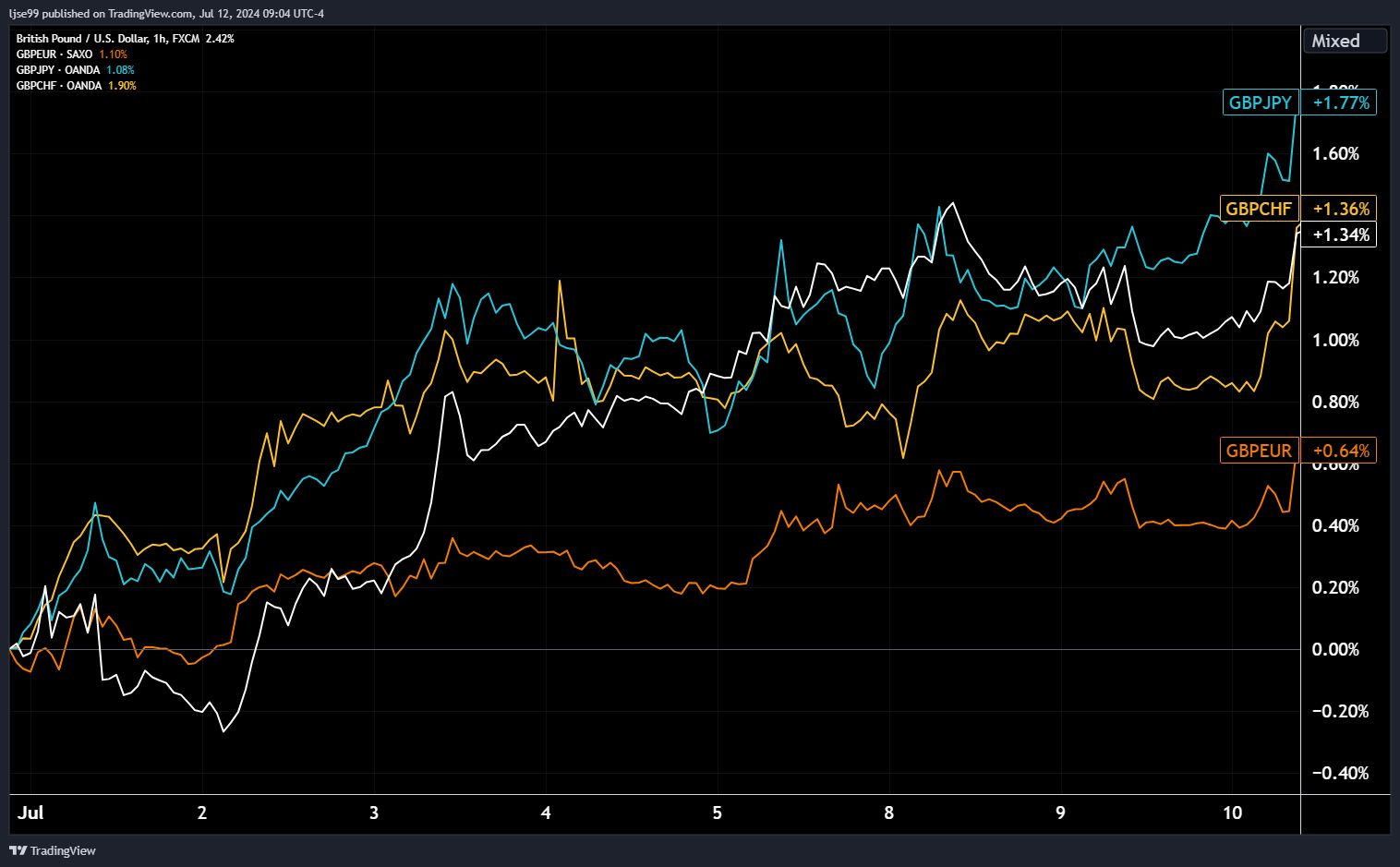

The UK had looked like a bit of a political basket case over the last few years, so the contrast of that to a new stable government is stark and has not been lost on international investors. The first port of call for market reactions to government policy, particularly the reactions of international investors, are the currency markets, where sterling has seen significant strength since the election results. Because the results were fairly certain, currency markets began to price-in a Labour victory at the start of the election week, so the chart below starts there. The blue line shows sterling against the Japanese Yen, the yellow line sterling against the Swiss Franc, the white line sterling against the US Dollar, and the orange line sterling against the Euro.

Figure 1 – Sterling versus major developed economy currencies – Source: TradingView, 2024.

Figure 1 – Sterling versus major developed economy currencies – Source: TradingView, 2024.

As the chart shows, sterling has been strong against the major developed market currencies, with inflows to British markets pulling up the currency value.

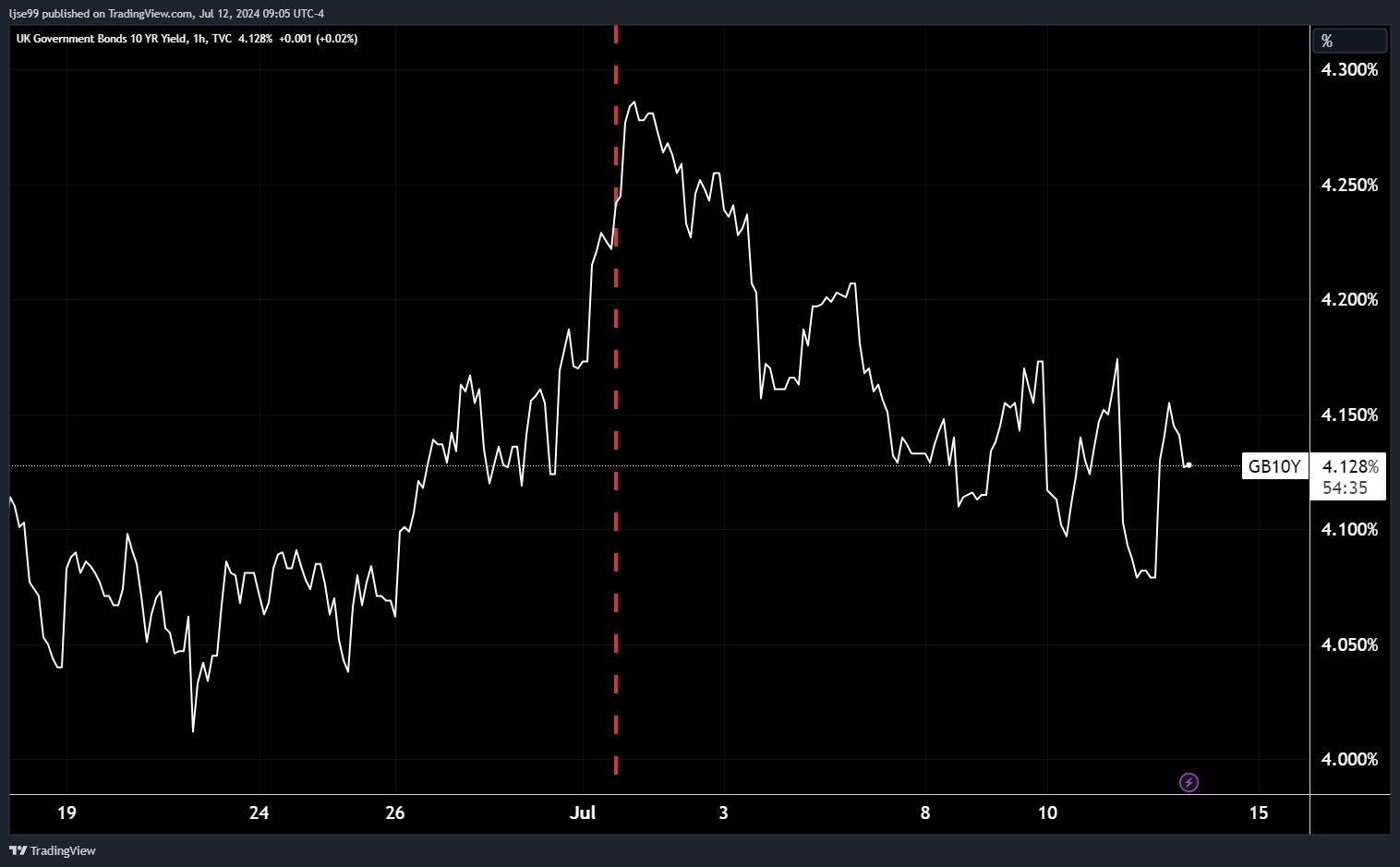

The next port of call is the bond market. If markets perceive a new government to be more stable and fiscally trustworthy, they should demand less compensation for risk and thus a lower government bond yield. Looking at recent moves in the gilt market, this is the result we find.

Figure 2 – 10-year UK Gilt yield – Source: TradingView, 2024.

Figure 2 – 10-year UK Gilt yield – Source: TradingView, 2024.

The chart above shows the yield on a 10-year gilt over the last three weeks, with the beginning of the election week marked by the red dotted line. Clearly, since the start of the election week gilt yields have come down as would be expected.

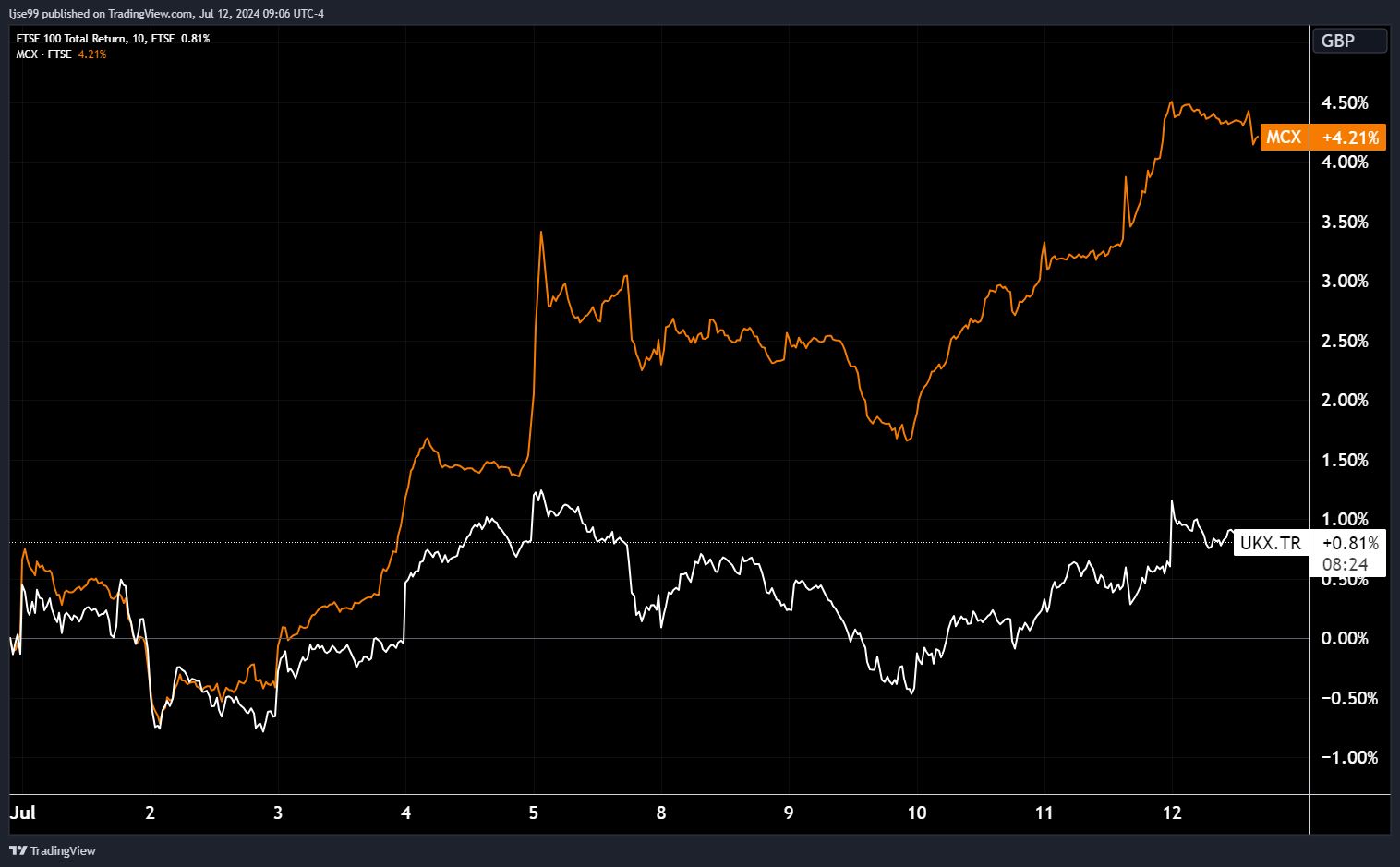

The final market we will examine is the equity market. The two main index groupings of UK equities are the FTSE 100 and FTSE 250, where the former are the largest 100 companies, typically international businesses, and the latter are the next 250 largest companies, typically domestically focused. An election has the largest impact on the prospects of domestically focused companies, so we should expect the FTSE 250 to outperform the FTSE 100 if investors see the election as being positive for the UK economy, and within the FTSE 250 we should expect domestically focused sectors to see the strongest performance. The chart below shows the performance of the two indices, starting at the beginning of the election week. The FTSE 100 is depicted by the white line and the FTSE 250 by the orange line.

Figure 3 – FTSE 100 & 250 returns – Source: TradingView, 2024.

Figure 3 – FTSE 100 & 250 returns – Source: TradingView, 2024.

As predicted, the FTSE 250 has outperformed the FTSE 100 over the period, with a pronounced spike in returns on Friday the 5th, the day election results were confirmed.

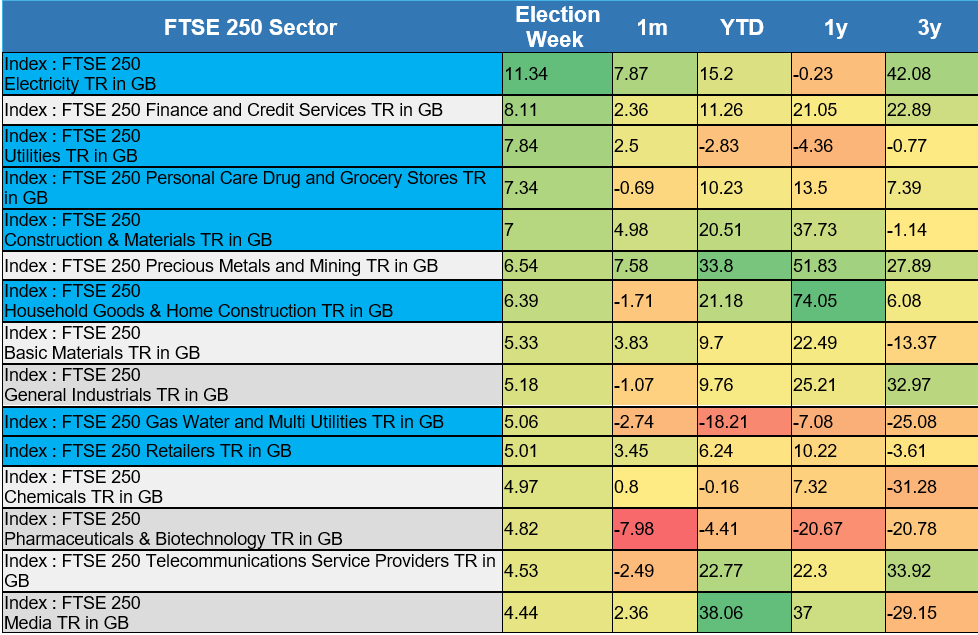

When breaking this down on a sector basis, we see that of the 15 top performing FTSE 250 sectors that week, 7 are industries that are very domestically focused (highlighted in blue).

Figure 4 – FTSE 250 sector returns – Source: FE Analytics, 2024.

Figure 4 – FTSE 250 sector returns – Source: FE Analytics, 2024.

The strong performance of construction & materials and household goods & home construction sectors is notable, as house building is a key priority of the Labour government – markets are taking this seriously and pricing it into equity valuations.

Market reaction to the French election result

Moving to France, where markets have been less than enthused by the results, to put it mildly.

France no longer has the Franc as an independent currency, meaning changes in the value of the Euro are not a pure proxy for changes in sentiment towards France, however as the second largest economy in the EU, France exerts a large weight on the value of the Euro, particularly on the day of the election result. The chart below shows the value of the Euro versus the Dollar on the day of the election, with the drop in value boxed in red.

Figure 5 – Euro versus Dollar – Source: TradingView, 2024.

Figure 5 – Euro versus Dollar – Source: TradingView, 2024.

As the chart shows, there was a significant uptick in volatility in Euro currency markets. This volatility isn’t restricted to currency markets, with equity markets across Europe seeing increased volatility, particularly when compared with UK equity markets. The chart below from Bloomberg shows the volatility of UK and European equity markets, with a clear spike during the election.

Figure 6 – UK and European equity volatility – Source: Bloomberg, 2024.

Figure 6 – UK and European equity volatility – Source: Bloomberg, 2024.

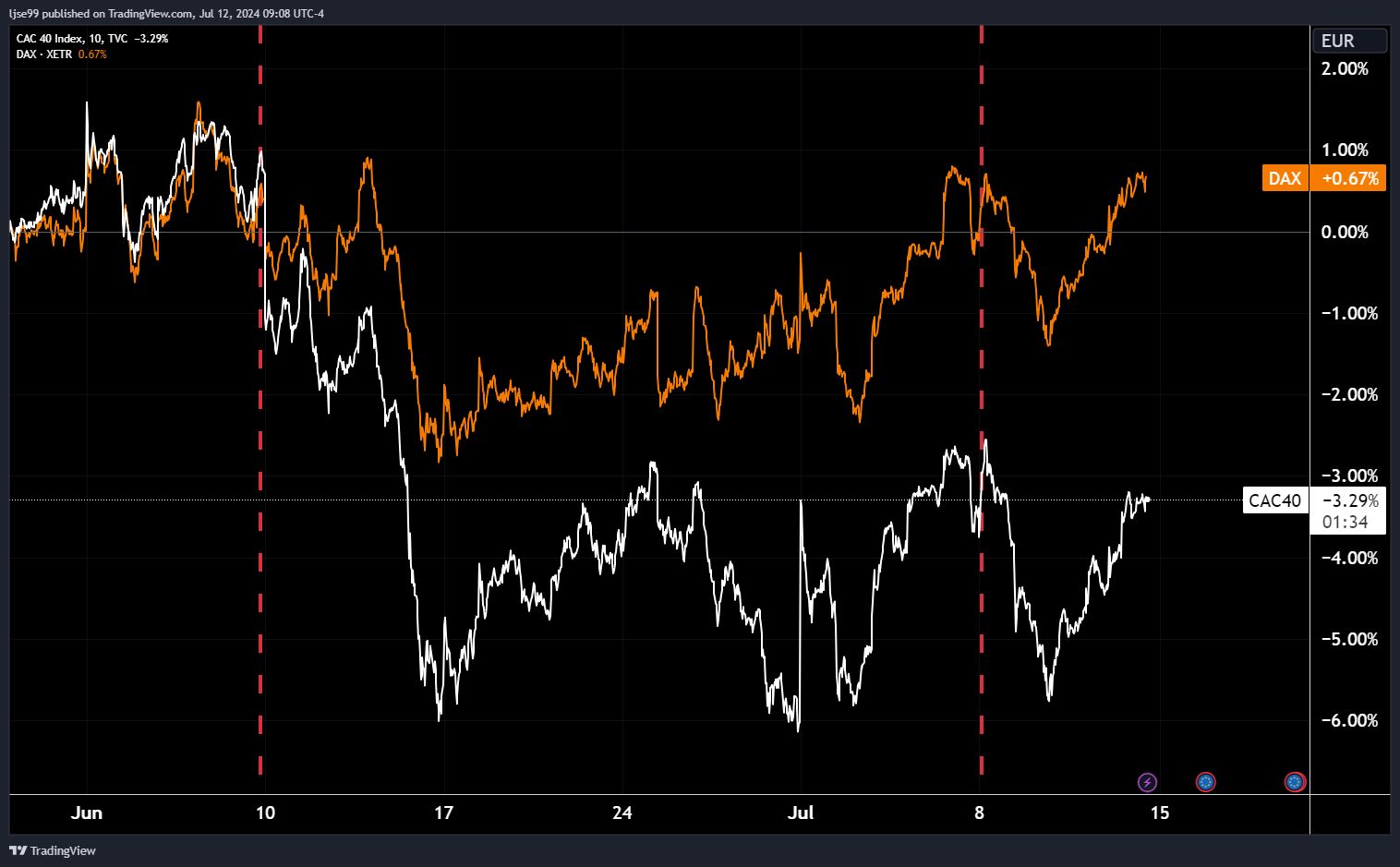

The chart above shows European equity volatility, but when breaking that down to look at the performance of French equities we see that much of this volatility has been caused by downwards moves in French markets. The chart below shows the returns of the French CAC 40 index in white and the German DAX 30 index in orange, with red dotted lines marking the calling of the election and the results of the election.

Figure 7 – French and German equity returns – Source: TradingView, 2024.

Figure 7 – French and German equity returns – Source: TradingView, 2024.

While German markets have moved broadly inline with French markets, downward movements have been less pronounced in Germany and recoveries weaker in France, with French equities exhibiting overall higher levels of volatility.

Finally, in fixed income markets the risks posed by the incoming French government are already being priced in, with bond investors demanding a premium to own French debt versus safer German debt.

What does this all mean going forward?

Looking purely from a market perspective these results are unambiguously good for UK markets. Valuations in UK markets have been particularly low since the 2016 Brexit vote and the subsequent political uncertainty, while France has attracted much inbound capital that would likely have landed on our shores. For so long as France remains politically unstable this is likely to reverse – we have already seen large Japanese and Taiwanese bond investors, primarily insurers, pull away from new French bond issuances and start to trim their holdings.

Outside of the France vs UK capital attraction comparison there is also the question of the FTSE 250, which having already got off to a good start looks primed to continue its strong performance – caveated with the fact that external factors, like a global recession, could easily blow things off course. Should the Labour government successfully implement their desired planning reforms and even get close to their target of the highest GDP growth in the G7, smaller UK companies can be expected to see material improvements in their business fundamentals, and with international investors finally giving the UK serious consideration, should also see the stock price gains to match. We remain cautiously optimistic for future UK market prospects.

If you have any questions about your portfolio please don’t hesitate to contact your adviser.

Arrange your free initial consultation

This market update is for general information only, does not constitute individual advice and should not be used to inform financial decisions.

Past performance is not a guide to future returns. Investment returns are not guaranteed, and you may get back less than you originally invested.